1-Page Summary

The failure of Enron in the early 2000’s is one of the largest bankruptcies in US history (with Lehman Brothers in 2008 as the largest). Its accounting scandal led to Enron’s bankruptcy as well as the dissolution of Arthur Andersen, one of the big five accounting firms. Shareholders were wiped out, and tens of thousands of employees left with worthless retirement accounts.

Today the name “Enron” still evokes a reflexive repulsion, a feeling that these were simply bad people doing illegal things. But, we think, that’s in the past. Surely we’ve evolved as a society, and by thinking hard enough, you or I can avoid these problems.

In reality, when you dig into the details, Enron’s downfall is the predictable mixture of human greed, poorly structured incentives, and lack of sanity checks when everyone has their fingers in the pie.

You might be surprised to learn that most of Enron’s accounting tactics were not technically illegal at the time - they were actually publicly celebrated for being financial innovations. Shareholders, employees, investment bankers, and accountants all benefited from the situation and enabled Enron for years. They only stopped when it became untenable.

The most important takeaway from The Smartest Guys in the Room is to understand the key enabling conditions for Enron’s deception. When multiple conditions mutually reinforce each other and create positive feedback loops, a massively outsized result - a lollapalooza - can happen.

These are also the warning signs you can use to detect unstable situations and desist from bad behavior.

Accounting practices that disguised the fundamentals

The root of Enron has to be the accounting tactics that enabled deception. They let Enron book more revenue than they actually earned; keep losses and debt off balance sheets. If these were disallowed, the money-losing state of Enron would have been apparent far sooner.

- Mark-to-market accounting allowed booking the total value of a deal immediately, rather than spaced out over time.

- Complicated SPE deals allowed Enron to borrow money while keeping it off their balance sheet

- One-time asset sales were booked as recurring revenue

- Deals that were actually dead were fictitiously kept alive to avoid a writedown that quarter

All this structure became so convoluted that no one totaled up the big picture. No one pieced together the dependencies between Enron’s deals, and how the dominoes would fall if Enron’s stock price fell.

Lesson: Resist the temptation of clever accounting tricks that mislead on fundamentals, even if they’re technically legal. You may eventually deceive even yourself on the true fundamental strength of the situation.

Poorly constructed compensation structures that rewarded unprofitable behavior

A pattern of Enron’s compensation style was to reward short-term behaviors (like stock price or closing deal sizes) without concern for long-term value (like profitability). And according to the book’s author, Skilling happily fed greed, believing it was the best motivator for performance.

- Deal makers were given bonuses for the deal value when it closed, not on the generation of actual cashflow. With optimistic projections, deal makers got paid for bad unprofitable deals.

- Employees got bonuses for short-term stock prices, thus incenting bad behavior to prop up stock price.

- Senior managers like Skilling got large bonuses for stock performance. This prompted over-optimistic projections to Wall Street, which intensified the speed of rushing into bad businesses (Enron Broadband) and created end-of-quarter scrambles to make earnings.

Lesson: Make sure your compensation structures align with the fundamental goals of the business, and that there are balancing check points

Believable guiding visions

These party lines began with good intentions, but as Enron slipped into a gray zone, they helped justify bad behavior.

Enron saw itself as revitalizing an industry populated by dinosaurs and bringing efficiency through privatization and free markets. With a missionary

Andy Fastow’s department saw itself as a financial wizard, pushing the boundary of possibility while staying within the lines of GAAP accounting. They were just playing the rules of the game.

Stakeholders/watchdogs overlooking bad behavior as long as they were profiting

People who could have stepped in and intervened didn’t, often because they had a large personal stake in Enron’s success. Further, the more Enron became a success (like in terms of stock price or deal flow), the more beholden the stakeholders were to Enron.

- Shareholders (employees and the public in general) didn’t look very hard, as long as the stock price rose and employees got bonuses. Why stop the party?

- Enron’s accountants (Arthur Andersen) couldn’t lose Enron as a client (Enron kept accountants waiting in the wings), so they tolerated their practices despite internal skepticism. Furthermore, Enron gave many Andersen accountants cushy jobs.

- Investment bankers earned large fees from Enron’s complicated deals, even when they knew they were skirting the intent of the law. Bankers who ran bigger deals got promotions. They competed for Enron’s business.

- Buy-side analysts at banks who were supposed to be independent were strongly pressured to give buy ratings, since companies would only work with positive banks.

- Short sellers were a useful counterforce, since they had a large incentive to expose wrongdoing.

Lesson: Correct for your own incentive bias when you analyze a situation.

Looking to others believing they had done their due diligence

When you have multiple reputable people on board, everyone thinks everyone else has done their diligence. Surely all these other people can’t be wrong! In reality, no one has done their diligence.

- Employees thought the board and accountants would keep bad behavior in check, and thought public markets were heavily incented to detect bad behavior.

- The board trusted the internal risk department, which in reality was a yes-man and thought their only job was to sign off on deals.

Lesson: Don’t trust other people’s due diligence. Assume they have the worst possible incentives to overlook problems. Do your own due diligence from first principles.

Big bets on businesses that failed

According to the author, the accounting tricks were meant to be short-term bridges to the real new money-makers: Enron Energy Services (retail utilities) and Enron Broadband.

Enron plowed a ton of money into these businesses, in typical Enron “move fast and go big or go home.” Their read of the market and industries was wrong.

Enron’s optimistic promises to Wall Street created a situation where Enron had to deliver fast on businesses, or else their stock price would plummet.

Lesson: Don’t excuse bad practices as temporary measures until your saving grace comes around.

Complex dependencies that required progressively bigger risks or face complete failure

Enron built layers of financial dependencies in a constant push to raise stock prices. In essence, it kicked the can down the road, hoping that salvation would come at some point.

- For example, Enron’s mark-to-market accounting might put the value of a 20-year deal down as recurring revenue in one quarter. Wall Street expected this to be real recurring revenue, which meant Enron had to book larger deals that had bad long-term prospects to keep up appearances.

Here was the nightmare scenario (that materialized):

- Enron’s stock price was high because of misleading accounting and overoptimistic projections.

- If Enron ever missed earnings, its stock price would fall.

- If its stock fell, its SPE deals would unwind (since they were predicated on Enron stock prices), causing Enron to have to book massive debt on its balance sheet or issue new shares. This would cause further stock price falls.

- This increased debt would cause a downgrade of Enron’s creditworthiness to junk status.

- This would trigger provisions in Enron’s debt agreements to pay back loans early, and trading partners to demand cash collateral.

- Since Enron didn’t actually have cash, its ability to pay would progressively worsen, causing trading partners to withdraw and further decrease revenue.

- This would cause bankruptcy.

Lesson: Don’t create scenarios where you kick accountability down the road and bet on a big salvation moment. Take moves to de-risk moment to moment, and take a big write down earlier. Be even more wary if this is an existential risk, since for the sake of staying alive you might take more desperate steps.

An unwillingness to consider the worst case scenario seriously

Because of such strong incentive bias, social proof, and self-consistency bias, Enron managers refused to believe that the stock price would ever fall and trigger the nightmare scenario.

Lesson: Seriously consider the worst case scenario, and think about ways that you can mitigate this.

Bad appointments to senior managers

Generally, promoting people who had the wrong kind of ambition (more to themselves than to the fundamental health of the company).

- Andy Fastow, known for experience creating financial structures rather than financial prudence, was promoted to CFO.

- Ken Lay was more interested in being a public figure than in managing the business.

- The board was weak, filled by Ken Lay with people who had reciprocal relationships with Enron.

Lesson: Hire people with the right kind of ambition, who want to grow the long-term success of the company (and are incented correctly).

Punishments for dissent/skepticism

Internally, Enron skeptics were punished for voicing discontent or blocking deals. They were reassigned to less glamorous parts of the company or publicly humiliated on their failure (like Rebecca Mark).

- Enron partners (accountants, bankers) who voiced discontent lost the deals. Enron managers even strongly encouraged the dismissal of employees who added friction to deals.

- Skilling had a tactic of making people feel dumb for asking questions. “All the data is out there. If you don’t get it, you’re just dumb.” Naturally, in the heady times of the dotcom boom, people didn’t want to look dumb or be wrong, in case Enron turned out to be a huge success.

Lesson: In your search for the truth, put aside the centering of your ego around being smart. If something seems too complicated for you to get, it’s probably not your fault - keep pressing.

Enron's Beginning and Promise

The Smartest Guys in the Room chronicles the history of Enron, from beginning to end. Putatively, it began with good intentions and a believable vision. Then, as it focused on short-term stock prices, it became corrupted by deceptive accounting, making more egregious bets.

Ken Lay Sees an Opportunity

Ken Lay, founder and CEO of Enron, believed in efficient markets. The 1970s energy crisis caused natural gas to become deregulated. Lay saw an opportunity to profit from this deregulation.

Lay had served in various roles in gas companies before heading Houston Natural Gas (HNG) in 1984. His vision was to control a large fraction of pipeline which would allow better negotiating leverage.

Larger Omaha company InterNorth, in danger of being taken over by corporate raiders, wanted to defensively increase its size and debt load. It acquired HNG in 1985, with terms very favorable for HNG. Ultimately, Lay gained control of the board and became CEO of the company, renaming it Enron.

Things didn’t immediately work out quite as well as Lay hoped. A glut of gas on the market depressed prices and put Enron’s long-term gas contracts underwater. Management of the combined entity was tough, riddled with politics. As a public company, Enron was desperate for real earnings. It turns out for all his enthusiasm, Lay didn’t personally have strategic insights into how to create a new business model in this new deregulated world.

Enron Builds a Futures Market

In this strategic vacuum, a consultant had an answer.

In 1987, Jeff Skilling, a McKinsey consultant who worked with Enron, envisioned Enron building a futures market, turning natural gas into a commodity (then a novel concept).

Put simplistically, Enron would be the mediator between gas producers and gas buyers, with Enron earning the spread.

Enron was able to loan gas producers more money than banks, because it knew the clearing price of the gas. So producers signed contracts to supply gas to Enron, in exchange for upfront money to develop reserves. Enron could then trade the future contracts, just like oil futures.

Enron’s physical assets, ability to actually deliver gas, and its history and reputation gave it an edge over Wall St competitors who later entered the industry.

Securitization of gas lifted capital and balance sheets as constraints on growth. Selling its loans allowed Enron to eliminate debt from balance sheets and get cash to grow further.

This later became Enron Capital and Trade Resources (ECT) and by 1996 it made $280 million in EBIT, more than 20% of Enron’s earnings.

Enron International

The Enron International arm began in Teesside in the UK, with a natural gas cogeneration plant built in 1991. This plan supplied both electricity and heat to the local area. This was a successful project, prompting energy companies to ravenously seek similar deals in developing economies.

Rebecca Mark headed Enron International. Fueled by a compensation scheme that rewarded closing deals and not actually building the businesses, Rebecca Mark globetrotted and closed deals in dozens of countries. She positioned Enron as the “solver of the unsolvable problem.” She was hungry to come up with projects bigger and better than Teesside.

The projects were often troubled. The largest scandal was in Dabhol, India. A province struck a deal very favorable to Enron, guaranteeing a long-term purchase of highly priced energy. The Indian population revolted, seeing it as rapacious globalization. This stymied development for years.

Furthermore, the financing for projects was often unclear. Enron International hoped the funding they would come from non-Enron sources, but sometimes Enron ended up guaranteeing the debt.

Enron International fed Ken Lay’s desire to hobnob with international luminaries like Kissinger and heads of state, making it less likely to be scrutinized.

By 1996, Enron International accounted for 15% of Enron’s earnings.

Leadership Changes

Rich Kinder

In 1996, Enron COO Rich Kinder was expecting the CEO job. Around this time, Ken Lay was expected to go into politics, but he knew he wouldn’t get a political appointment under Democratic Clinton. Lay also didn’t respect the work that Kinder did. So Lay ousted Kinder, who founded energy company Kinder Morgan afterward (still a healthy company today worth around $45 billion as of time of this writing).

Kinder was a voice of reason within Enron, expecting discipline and skeptical of bad deals. After the collapse of Enron, some suspected Enron could have saved itself had he been appointed CEO.

The RIse of Jeff Skilling

With the power vacuum, Skilling (head of Enron’s trading operations) maneuvered into the COO role, basically by threatening to quit if he didn’t get it. This triggered a number of changes:

1) The focus shifted to trading as the core of Enron’s business. Physical assets that actually dealt with supplying energy were sold off.

- EOG (Enron Oil and Gas) was spun off. It still survives today as a public company, EOG Resources.

2) Enron’s trading scope expanded outside natural gas. Their aim was to become “The World’s Leading Energy Company.” They expanded into electricity, and they engaged in plant deals from gas plants to water, steel, and paper. The promise was huge - if Enron could create an electricity-trading business and claim 20% of it, the payoff would be enormous.

- But they overextended, believing the markets were more similar to gas than they really were. For example, as an outsider to electricity, Enron was feared as the big player that incumbents shouldn’t partner with.

3) Enron International head Rebecca Mark was sidelined and knew she wouldn’t rise further in management. She decided to buy a British water utility, forming the company Azurix. (This would later end in failure, described in a later chapter.)

4) Skilling set up a Risk Assessment and Control (RAC) department, which publicly was believed to be watertight and having strong veto power over risky deals. Stock analysts believed Enron had tight risk management capabilities, which gave Enron the leeway to take on more risk than other companies.

- In reality, RAC was just a yesman, with a weak manager in place who didn’t fight against bad deals.

- RAC staff also faced strong pressure to close deals to hit quarterly numbers. Enron’s staff had a peer review system that was a key component of promotions and compensation. Deal originators within Enron threatened poor peer reviews for RAC peers who didn’t approve deals.

Wall Street Expectations

Enron promised Wall Street 15% growth a year. This obsession with meeting earnings targets powered the deception that was later to come.

In 1997, Enron made $105MM, a 82% drop from 1996.

- Gas trading had become more competitive. Banks were making loans, and buyers were loath to sign long-term origination deals.

- Some earlier deals had turned out unwise and missed projections, requiring writedowns.

In this environment, where Enron made aggressive promises to investors, but had shakey core operations, it couldn’t resist the temptation to conduct fraud to meet numbers.

Enron's Bad Practices

The Start of Bad Practices

Trading companies are too volatile to reliably produce increasing earnings. So rather than claiming to be a speculation company, Skilling branded Enron as a logistics company, finding the most cost-effective way to delivery power from any plant to any customer. This provided cover for incomprehensible businesses.

Skilling feared that any appearance of losses would shatter the illusion of Enron being wizard risk managers, so fought hard to hide them.

Skilling’s obsession with Enron’s stock price and with meeting quarterly Wall Street targets got Enron addicted to bad business practices:

- Skilling would ask analysts, “what earnings do you need to keep our stock price up?” This was the number he targeted, regardless of whether it was conceivably achievable by the company.

- Quarters would end with execs scrambling to fill “holes” in the company’s earnings and cover up losses. Deals scheduled to close on later timelines were accelerated, at the expense of costly long-term concessions for Enron.

- Enron used mark-to-market accounting for its deals, which allowed booking the total value of a deal immediately, rather than spaced out over time. They practiced this throughout the business, including on private equity and venture capital investments.

- Mark-to-market requires assumptions about the future performance of deals, and naturally they skewed optimistic. These assumptions were not visible to the public.

- Earnings projections were re-examined and made more optimistic.

- Even if deals failed or were dead, they delayed recognition of those losses in a particular quarter by pretending they were still alive.

In effect, all these dealings created fictitious cash flow and profits when they were really dealings with itself - and at some point the house had to collapse.

Andy Fastow Brings New Convoluted Deals

In 1998, the rise of Andy Fastow to CFO brought complicated structured-finance deals that gave Enron cash that could be kept off the books. The goal of these deals was to keep fresh debt off the books, camouflage existing debt, or book earnings or cash flow. They allowed Enron to borrow money while disguising their real debt.

In summary, Enron took out large loans and made them appear like cashflow. Enron had to pay these loans back over time, but it didn’t actually have real cashflow. So it would take out further loans to pay back earlier loans. This is the corporate equivalent of starting new credit cards to pay back old credit card debt.

The types of deals included;

Special Purpose Entities

Special Purpose Entities (SPEs) are meant to be independent legal entities that fulfill a narrow objective, like purchasing assets/securitized assets from other companies. They are structured to be separate legal entities from the main firm, to protect the firm from financial risk.

Enron abused the SPE structure to inflate earnings and hide losses. In summary, Enron used these SPEs to raise debt to purchase assets, without the debt or assets showing up on their financial statements. Enron would then sell assets to these funds and book it inappropriately as cash flow. Later, Enron would also use SPEs to hide troubled assets that were falling in value, which meant losses would be kept off Enron’s financial statements.

As long as 3% of the capital in the SPE came from an independent source and was at risk (not guaranteed), then the SPE qualified as independent. Thus Enron could fund 97% of the capital from raising debt, but not report this as debt on their balance sheets.

- In reality, the 3% of capital often came partially from friends of Enron employees, so they weren’t truly independent.

In reality, Enron gave guarantees to lenders, including guaranteeing a debt-like return while Enron kept the real return.

- Further, the debt was rarely supported by the true value of the asset, since it was based on unreasonably optimistic assumptions about the success of the asset.

Further, sales of the assets could be booked as operating income. So it looked like Enron had sold something and booked cash flow. But there was a big wad of additional debt that had to be paid back.

- Further, this operating income only appeared once - Enron couldn’t claim that cash flow in future years. So Enron promised public markets growth of real underlying earnings, but was actually filling it desperately with one-time sale deals.

Minority Interest Transactions

A majority-owned Enron subsidiary (Entity A) purchased poorly performing Enron assets. A new allegedly independent Entity B took out a bank loan to purchase a minority interest in Entity A. Entity A then loaned Enron these funds from the sale to Entity B.

With this structure, it appeared that Enron received funds from an affiliate, as opposed to from the bank that loaned Entity B. Thus Enron didn’t book debt for the transaction, and Enron booked funds as operating income!

Ostensibly, the value and earnings of the assets would pay back the debt. However, if the assets were insufficient to pay back, Enron would issue stock or pay cash to Entity B. These guarantees made the arrangement much more like a loan than a true equity purchase.

Example: Project Nahanni: Enron borrowed $485MM in debt and $15MM in equity to buy Treasury bonds, sold the Treasury bonds, and booked this as cash flow.

Prepay

Enron would agree to deliver natural gas/oil to an independent offshore entity. The entity would pay Enron upfront for these future deliveries, with money it obtained from a lender. The lender would then agree to deliver this commodity to Enron; Enron would pay a fixed price for these deliveries over time.

In reality, this was little more than a loan:

- Take the commodity out (it just circles from Enron to entity lender to Enron), and you have a pure loan with interest.

- The entity was set up by the lender.

- These prepays weren’t accounted for as debt, but rather trading liabilities offset by trading assets.

Enron was perennially short on cash, so instead of using operating cash flow to pay them back, it used fresh prepays to replace earlier ones. This is another example of Enron’s pattern of using increasingly complicated vehicles to cover for previous shortfalls.

This Was All Done in the Open

Contrary to popular belief, many of these deals were not secret, but rather publicly revealed and boasted about.

Third parties internal (Arthur Andersen) and external (analysts) applauded the deals for their financial ingenuity. Banks participating in the deals earned large fees.

Fastow, who saw himself as a savior of the company, inappropriately participated in these deals himself, providing the 3% independent capital for the SPE. In Fastow’s view, these were “just commissions,” and Enron owed him for saving the day.

Enron’s Chief Accounting Officer Rick Causey was meant to keep Fastow in check, but he saw his job as facilitating Fastow’s transactions.

By the end, Enron owed $38 billion, of which only $13 billion was on its balance sheet.

Enron Digs a Deeper Hole

The bad practices were begun to hide losses and prop up stock price. As the fundamental core of Enron failed to yield actual revenue, Enron felt forced to expand its deception, putting off its day of reckoning to later.

Enron’s Two Big (Failed) Bets

All the financial machinations around SPEs were meant as temporary measures while Enron bet big on its next two major businesses. Both of them, however, sustained massive losses.

Enron Energy Services - Retail Utilities

Enron’s historical bread and butter was large wholesale contracts with commercial buyers. But it believed there was a coming wave of deregulation, where federal/state governments would release municipalities from local monopolies to allow the free market to drive prices down. Enron could then sell directly to businesses and homes.

In reality, the federal government wasn’t interested in intervening in state affairs, and only a few states started pilot programs toward deregulation (New Hampshire, Pennsylvania, California).

In the few hotspots it could work in, Enron campaigned aggressively to recruit consumer households to sign up, promising lower utility costs. However, the local suppliers fought back, pulling their political strings and running ads against the big guy coming into town.

In the end, few consumers really signed up for Enron’s services - 50k in California (1% of the market) and 300 in New Hampshire.

After the residential failure, Enron targeted businesses. This was enticing - a big company spends millions a year for light, heating, and cooling. Couldn’t Enron get a share of this?

The commodity part of this business was actually a money-loser - Enron’s hope was that it would make money on contracts to reduce energy costs and increase efficiency.

Enron signed lots of deals at below-market utility rates - Ocean Spray for a $116MM 10-year agreement; Owens Corning for a $1B 10-year contract. The “total contract value” (TCV) was $8.5 billion - an impressive number on the surface. But TCV bore no relation to revenue or profits - it merely represented the cost of all the utility needs a customer had outsourced to EES.

Regardless, this new TCV became the sought-after metric of the day, since it gave the appearance of Enron signing big business. As usual, Enron deal makers were given bonuses on total TCV and the projected profitability of the deal (which were wildly optimistic). Naturally, a lot of bad deals were signed very quickly.

The operational requirements of this new business put Enron out of its depth - servicing customers directly required customer service, attention to detail, and hard manual work that Enron executives referred to derisively as “butt crack” work.

Enron tried to argue that efficiency improvements would help them make the deals profitable, but soon it became clear those efficiency improvements wouldn’t pay for themselves.

Enron Broadband

In 1999, Internet stocks were overheated. Put “broadband” in your company somewhere, and the stock price would rise without tying to fundamentals.

- Skilling calculated that every $1 invested in broadband would pay back $20 in market capitalization.

Skilling promised such large returns that the division was strongly pressured to make deals happen. They burnt a lot of money ($500MM a year) trying to find a valuable business plan.

The larger vision was that broadband might ultimately become a tradable commodity, like natural gas or oil. But this vision failed to meet reality:

- Physical technicalities got in the way. Internet lines were set up so sharing bandwidth wasn’t possible. In one sense, internet pipes were parallel pipes that never intersected.

- Enron promised that it was inventing new routing technology that would enable bandwidth sharing, but this never made it out of the lab.

- Meanwhile, the incumbent telephone companies were uninterested in hooking into Enron’s market. This would turn bandwidth into a commodity that would cut into their control of markets.

Enron even began partnering with Blockbuster to build content streaming services. Its rosy projections made napkin-calculations on how many cities they would enter, the market share they’d have, and the # of movies users would buy. In classic Enron fashion, it booked $110 million in profits from this deal immediately, before anything had materialized.

The reality of executing on content streaming was difficult. The content owners had massive leverage and were wary of entering a distribution medium they couldn’t control. Streaming from the Internet to the TV required expensive special boxes. And incumbent DSL providers controlled access to the last mile and were tough in negotiations.

The trials were tiny - 300 households involved - and the ultimate real sales from this were laughable, in the dozens of dollars. An Enron executive handed the business manager $5 and said “there, I doubled your revenue.”

The deal fell apart months after announcement, with Enron claiming Blockbuster hadn’t lined up content providers like promised.

Even though the failed deal should have been written down as a loss, Enron reasoned that it should actually be a gain - Enron would no longer have to share the proceeds!

Unfortunately, both Enron Energy Services and Enron Broadband bets were off the mark. Enron spent billions on unprofitable projects. This put Enron in an impossible position - having spent all that money and raised expectations, there was no room for failure. They could only hide the massive losses through more machinations.

Andy Fastow Profits from Deals

Meanwhile, CFO Andy Fastow positioned himself aggressively to profit from Enron’s deals.

The cash-losing EES and broadband divisions chewed through so much money that Enron became even more dependent on Fastow’s deals to avoid appearance of losses.

Fastow set up private equity funds (named LJM) that would be the 3% “independent capital” for the SPE deals that Enron was addicted to.

- As a part owner, he would earn “normal fund returns” like management fees and 20% of carry.

- He also invited select Enron lieutenants and friends to participate - ultimately, they would get an 180x return.

The possible conflict of interest was obvious to most concerned - Enron employees in the know, the board, and LPs of Fastow’s funds. But they all stepped out of the way for their own reasons:

- Enron employees were worried about being berated by Fastow and having their ratings punished. Objectors were publicly transferred to other departments out of Fastow’s way.

- The board was comforted by assurances that all deals would be reviewed by the Chief Accounting Officer, and Fastow could be removed at any time. (In reality, the CAO was a rubber stamp.) Further, the board were likely emboldened by the stratospheric rise in Enron’s stock price in the late 90s.

- LPs wanted access to Enron deals, and Fastow made clear that participation in his private fund was required to stay in his good graces.

Many of the deals were rigged in LJM’s favor - Enron essentially guaranteed LJM against losses and bought back bad assets at inflated prices.

- Why would Enron do such bad deals? LJM’s job was to make Enron look good - warehouse troubled assets, getting them off Enron’s balance sheet and allowing Enron to book profits and cashflow. Enron needed LJM so desperately to keep up appearances of earnings that it structured great deals for LJM.

- The deals were structured in a way that implied the fundamental belief that Enron stock would never fall.

- Some deals were outright fraudulent - three Natwest partners deceived their employer on the value of portfolio assets and arranged transactions to pocket $2.4 million each.

Fastow set up 3 of these funds, and was angling for a 4th that would raise $1 billion and be his ticket out of Enron. (At the end, Fastow’s total take would reach $60 million.)

Energy Traders Take Bigger Risks

Meanwhile, the energy traders were making lots of money in the volatile markets. They were one of the few really profitable centers of the company, giving credence to Skilling’s vision of a next-generation, asset-light energy company.

In the early inefficient markets, traders used fundamental research to make smart trades - like finding dam water levels to estimate future water prices or using weather to estimate fuel prices. Money came so easily they were bewildered.

They made even more when they launched Enron Online - a virtual trading floor for energy futures.

- Enron served as the marketmaker, representing both sides of the trades. This dramatically increased the capital requirements (the danger will become apparent later).

- Its dominant position, as well as proprietary info on what outside traders were doing on their platform, allowed Enron to possibly manipulate markets to move prices in its favor. Enron supposedly did 25-50% of the trades in gas futures and electricity.

- They justified manipulating prices as just mere supply and demand - “traders don’t determine long-term price. No one had to use EOL - it wasn’t their fault others couldn’t come up with anything better.”

Within Enron, the traders saw themselves as the intellectual elite and the salvation of the company, since they were actually making money.

Enron Trading and California’s Blackouts

Enron traders participated in California’s partial deregulation of electricity, becoming enmeshed in the controversy around California’s blackouts and emergencies.

The regulatory change: California opened electrical grids to competition in a market, where electricity had previously restricted it to certain providers with controlled costs. Utilities had to sell off their generating facilities and buy power on the open market.

But the regulation was partial - price caps were instituted; rates to consumers were fixed; and utilities were precluded from longer-term agreements that might have allowed hedging and reduced spikes in prices.

- Other rules (made with good intentions): if a power line became congested, companies would be paid fees to relieve the congestion - even if there wasn’t enough demand to cause congestion in the first place.

Enron took advantage of the rules to manipulate markets, to the detriment of consumers:

- Energy producers kept power plants off to spike prices.

- Electricity rates were tied to the price of natural gas, which Enron was also in a natural position to control.

- Enron got paid for electricity through routes that didn’t have the bandwidth to transmit it. The utilities then had to hustle to find last-minute power at high prices.

- Enron submitted schedules reflecting illusory power demand.

- Enron would sell power as reserves without actually having it.

- Enron exported power from California and brought it back in desperate times (“megawatt laundering.”)

- The partners (out of state utilities, power suppliers) were happy to oblige because they made money too.

Ultimately utilities were forced to pay far more for power than they could collect from customers, who were still paying regulated rates. One incumbent went bankrupt.

Vicious cycle: because of this instability, power producers began refusing to ship to California. (Later the US Energy Secretary imposed a state of emergency, requiring marketers to sell to California.)

If Enron had a long-term view, it would have seen that California’s experiment needed to do well to make bigger business for it later. But it held destructive short-term views, like “other people are doing this too” and “California didn’t fully deregulate like we suggested so it deserves what it gets.”

Free market supporters claim that California’s partial deregulation set up a worse scenario than total deregulation, and California didn’t do enough to create enough electricity supply (for example, by removing price caps to incent development or realizing that hydroelectric power was subject to risk from low rainfall).

Ultimately Enron lawyers told the traders to stop.

Enron Trading Takes Bigger RIsks

Their hubris in energy trading led them to launch trading ventures in a host of other commodities - steel, paper, lumber, metals, bandwidth. Skilling thought Enron could be the market maker for everything! None of the others launched to much success.

They continued taking progressively riskier positions, breaking the trading limits.

As always, mark-to-market became a risk - they made their books look better through optimistic projections.

Long-term trades wouldn’t deliver cashflow immediately. So despite being one of the few profitable centers, the trading floor also became dependent on Fastow’s deals.

In 2001, Enron took a large short position on electricity (forecasting lower energy prices and less volatility due to the weakening economy and conservation).

Enron International is In Trouble

Meanwhile, former head of Enron International Rebecca Mark was in deep trouble at water services company Azurix.

With typical Enron hubris, Rebecca Mark thought water was easy and the incumbents were ancient. They would come in, make large deals, and figure out the details later. They also anticipated privatization of water supply, and a coming water crisis.

Immediately they ran into competition with two global heavyweights who competed aggressively for contracts to service municipalities.

Azurix was also in money trouble - the Wessex deal had cost a lot, and Enron saddled Azurix with large debt. So Azurix IPO’d in June 1999, raising $800 million at a stock price of $22 - despite people knowing Azurix obviously wasn’t ready to go public.

Now a public company, Rebecca Mark stressed the appearance of making big deals to buttress their stock value. In the few deals that Azurix won, they vastly overbid, largely out of desperation to signal momentum.

- Azurix won a contract in Buenos Aires, where the operations they inherited were so poor they couldn’t bill 40% of their customers and the facilities were lacking basic maintenance. It became clear Azurix would never make money on that deal.

4 months after IPO, Azurix had fallen to $13 a share; on a pessimistic earnings call in November, it fell to $8.

By the end of 2000, Azurix had less than $100MM in operating profit, down from $232MM at its start. Its debt load had quadrupled to $2 billion. Enron announced it would acquire the public shares at $8.375 a share.

Jeff Skilling, Rebecca Mark’s rival, took every opportunity to ridicule Azurix as a failed business model, in comparison to his asset-light “logistics” and trading businesses.

Enron believed that Azurix was so unimportant that if it failed, it wouldn’t have any effect on Enron. This later proved wrong. For instance, Enron had $1 billion of debt they were not clearly on the hook for.

(To Mark’s credit, Azurix at least represented real assets and cashflow - low, but cashflow nonetheless).

Enron’s Stock Price Rockets

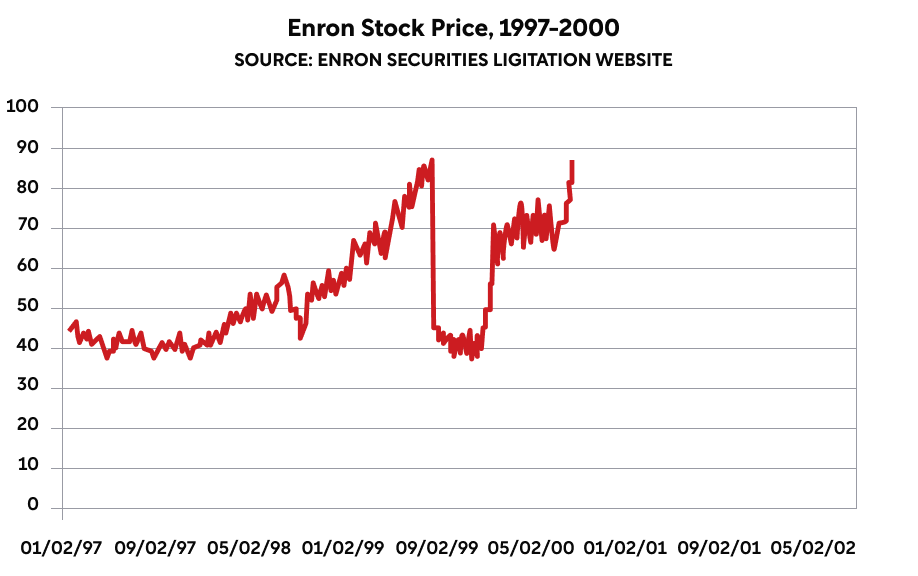

Despite all this trouble bubbling under the surface, in the heady period of 1999-2000, Enron stock exploded in price, reaching ~90 in Aug 1999 before being split 2:1, then doubling to reach 90 again in Aug 2000 for a market cap of $70 billion. It outperformed the S&P by over 200%.

This is a testament to how powerfully its accounting distortions disguised the true nature of the problems brewing.

- 2000 revenues showed $100 billion, 100% over 1999. Earnings hit $1.3 billion, up 25% per share.

Enron was paraded as a visionary company, building new businesses like Enron Online in the Internet era.

To the public, Enron only ever expressed certainty of being a juggernaut. Said Enron, it would inevitably own 20% of every major market, which meant its fledgling businesses were already worth billions, and should be priced accordingly. After such an announcement in their analyst meeting in Jan 2000, Enron’s stock rose 26% in a single day.

Enron employees started drinking the kool-aid. They thought they couldn’t make mistakes and were bulletproof.

(Shortform note: also consider yourself in this situation: Enron’s stock price has quadrupled in the past 2 years. How easy would it be to overlook bad behavior in these heady times?)

Cracks Start to Appear

Despite Enron’s best efforts to conceal their losses, by late 2000, skepticism started mounting. The dotcom bubble had fallen from its peak, and company fundamentals were being questioned.

On December 2000, Jeff Skilling was announced to succeed Ken Lay as CEO, taking place in February. This was already planned well in advance - his contract had a trigger - if he weren’t named CEO by end of 2000, he could leave and be paid over $20MM.

SPEs, Again

Enron embarked on new schemes to lock in gains while avoiding booking losses.

In 2000, SPEs called Raptors would buy underperforming Enron assets. If the assets continued to decline in value, the Raptors would pay Enron, thus giving Enron a gain that would offset the loss.

In reality, these transactions were grounded on Enron stock. This led to positive feedback loops:

- An increasing Enron stock price would allow further ability to keep losses from public view, which would in turn increase stock price.

- However, if Enron shares fell, the Raptors would be less able to pay back Enron, which would cause further share cratering.

By late 2000, the assets in SPEs declined in value, and Enron needed its stock to continue climbing to cover losses. Because the stock price stalled, Enron would have to declare losses, which defeated the purpose of the vehicles. An emergency solution cross-collateralized the four Raptors, allowing healthy vehicles to support sick ones.

Concerns Mount

There started to be mounting external and internal concern about the reality of the losses.

By spring 2000, the dotcom bull market was over. Analysts were now questioning business plans and looking for fundamental cashflow and revenue. Momentum investors were selling instead of buying.

- Stories ran about how energy companies used mark-to-market accounting, and no outsider knew the assumptions they used to book earnings.

- Short sellers were gaining credibility and wielding larger sticks. Investor Chanos was skeptical Enron’s broadband business could be doing so well when the rest of the industry was getting slaughtered.

More negative signs cast doubt on Enron:

- Unclear disclosures about dealings with a related party

- Lay and Skilling were selling shares

- Debt was climbing when Enron was supposed to be profitable

- No one could explain how Enron made money

- Redeployments/layoffs were happening at the broadband business.

- In April 2001, on an earnings call, Skilling famously called a skeptical short-seller an “asshole” for saying Enron was the only firm who couldn’t release a balance sheet or cashflow statement. Said a stunned analyst, “any CEO should be able to handle the hardest of questions from the most aggressive of shorts.”

In February 2001, an Enron accountant, Wanda Curry, saw that EES (the retail division) had over-optimistic valuations of deals and bad trades that, on inspection, actually put the division in the red by $500MM.

- Enron’s solution was to merge the trading losses with the wholesale traders’ profits, eking out a mild profit in total. However, Enron didn’t properly report the combination of the two.

In March 2001, this book’s author (Bethany McLean) published a landmark article, “Is Enron Overpriced”, which showed the public that professional analysts had no idea how Enron made money.

In May 2001, a researcher wrote a paper deconstructing Enron’s cash flow. Of Enron’s reported $4.8 billion in operating cash flow, $2 billion was from customer deposits (which would be paid back if energy prices fell); $1 billion was from a onetime sale of inventory, and another $1.5 billion was the result of prepay. This showed a dramatically different story than the idea that Enron’s cash flow was stable and recurring.

In July 2001, internal concern over LJM’s dealings with Enron prompted Fastow to sell his interest in the LJM funds to Michael Kopper, who left Enron to take over.

Even employees started questioning Skilling publicly: “You say we’re going to make half a billion a year. What’s your strategy?” Skilling replied: “that’s what you guys are for.”

The Dominoes Start to Fall

As a result, Enron’s stock price fell dramatically: from a height of $82 after their investor conference in Jan 2001, down to $68.50 in Feb 28 and $55 in March 21.

- Even in July 2001, when Skilling announced Enron had beaten earnings per share, share prices didn’t budge. The market had become too skeptical.

In August 2001, Skilling resigned as CEO.

- Reasons: The pressures of maintaining a rosy public facade while dealing with internal turmoil ate at him. For someone obsessed with the stock price, its decline represented a personal failure. He hated getting his hands dirty, and his job was now about fixing problems.

- Skilling’s resignation fueled suspicion that something was wrong inside Enron.

Ken Lay returned to a hero’s welcome, like the company’s savior. But having been a non-operator for years, he wasn’t helpful.

- He announced a onetime options grant of 5% of salary. The stock was at the bottom of the cycle, and “we want you to enjoy the ride back up.” The stock was at $38.

- He announced Greg Whalley, head of wholesale trading, as COO. Whalley quickly dug in and pressed for clear financials.

- Tidbit: Ken Lay himself was paying off creditors. Despite having a net worth at its peak in the 9 digits, he had “diversified” by taking out loans with Enron stock as collateral, and with terms to face margin calls at lower Enron stock prices. The loans were then put into ill-fated investments.

Here was the nightmare dominoes scenario - where all the intricately connected layers would fail because of their dependencies:

- If Enron missed earnings, its stock price would fall.

- If its stock fell, its SPE deals would unwind (since they were predicated on Enron stock prices rising), causing Enron to have to book massive debt on its balance sheet or issue new shares. This would cause further stock price falls.

- This increased debt would cause a downgrade of Enron’s creditworthiness.

- This would trigger provisions in Enron’s debt agreements to pay back loans early, and trading partners to demand cash collateral.

- Since Enron didn’t actually have cash, its ability to pay would progressively worsen, causing it to go bankrupt.

- Senior managers predicted the likelihood of this at less than 25%.

Enron's Final Moments

The nightmare scenario is more or less what happened at the end of 2001. Over a series of months, Enron collapsed, one step after another.

Internal rumors began circulating about issues at Enron.

- Accountants looking into the SPE deals realized that the falling value of assets in the SPEs, along with the falling Enron stock price, were going to become difficult to pay off. “It’s a bit like robbing the bank in one year and trying to pay it back 2 years later.”

- It was known that EES’s losses were being hidden in wholesale. In an employee letter: “This is common knowledge...and is actually joked about.”

The SPE Raptor deals ran into trouble.

- The Raptor deals became underwater by 9 figures, especially in the market hit after September 11.

- Andersen auditors realized they made an accounting error - Raptor restructuring had been booked as a boost in shareholder equity and needed to be reversed, costing equity $1.2 billion.

- This would be recorded as a simple equity reduction, rather than a restatement, which would admit mistakes and trigger SEC inquiries and lawsuits.

- COO Whalley argued to take the hit and clean up. They felt Enron would recover after cleaning up.

- To make the accounting look more favorable, Enron wanted the correction as a nonrecurring charge. Since this was originally booked as operating profit, this was grossly inappropriate. Andersen put up a fight, but ultimately Enron forced their hand.

On Oct 16 2001, Enron shared its third quarter report. They were sanguine as usual: “recurring Q3 earnings of $.03 per diluted share; reports nonrecurring charges of $1.01 billion...reaffirms recurring estimates.”

- The Wall Street Journal attacked the nature of the writedowns in a series of articles.

- Prompted by these articles, the SEC began an informal inquiry into Enron’s dealings with Fastow’s partnerships. Announcement of this sank the stock 20% to $20.65

- Oct 17: Moody’s announced it was placing Enron’s debt on review for a possible downgrade. It focused on 3 issues: negative operating cashflow, slow progress in asset sales, and more writeoffs involving Dabhol, Azurix, and broadband.

- Oct 23: Andy Fastow was interviewed about his income from the LJM deals. The next day, Whalley fired him.

On Oct 24, 2001, Enron was unable to roll its “commercial paper,” short-term loans used for day-to-day expenses. It had no operating cash.

- It desperately tried to make deals for cash - like opening up its books - but no one was willing to bite. It had to draw down $3 billion in backup credit lines.

- The last-ditch solution was to sell their pipelines, the only steady cash generator Enron had left.

- Enron’s trading also required credit to survive - trading partners would start demanding cash collateral.

Through this turmoil, Arthur Andersen began realizing how bad their work with Enron would make them look.

- Andersen had previously paid fines for accounting fraud at Waste Management - it had a cease-and-desist from the SEC from misconduct. In that case, Andersen’s records had provided regulators with plenty of proof - it wanted to avoid that mistake again.

- There was a shredding frenzy in both Enron and Arthur Andersen (following normal “document retention procedures”) until an official subpoena on Oct 26 forced them to stop.

- Andersen also saw major mistakes in Enron’s SPEs accounting, with the 3% not being truly independent capital. This meant the deals had to go back on Enron’s books.

Once dancing to Enron’s tune, the bankers realized their new leverage over Enron and took advantage.

- Beyond its credit line, Enron needed an extra $2 billion in cash. Banks refused to let it borrow the loans unsecured like before - now it demanded the only collateral remaining - the pipeline systems - and exclusive business with Enron for the next 18 months.

In early November, a possible savior came in a possible merger with smaller energy company Dynegy.

- For years, Enron took pot shots at Dynegy for being a tiny wannabe and threatened to steamroll it in every business line. The Dynegy CEO now saw a chance to get even, inherit its valuable trading operations, and vault his company to leading position in energy trading.

- The structure - Dynegy would buy Enron at market price. ChevronTexaco (26% owner of Dynegy) would provide $2.5 billion ($1.5 billion now, $1 on closing).

- In reality, this was undercapitalized from the start - Enron assumed that having ChevronTexaco onboard would be so reassuring its capital needs would shrink.

- Dynegy estimated it would boost earnings per share by 35%, with over $200 billion in revenue and over $90 billion in assets.

- The traders weren’t happy about this deal. They had already felt they were carrying Enron, and now they felt small dumb Dynegy was unworthy of buying Enron. The traders banded together to demand bonuses in cash upfront, or they’d blow up the deal.

Meanwhile, the SEC required that Enron disclose the Fastow partnerships and restate its earnings on Thursday November 8.

- Also, all three ratings agencies cut Enron to one notch above junk by Nov 5. Shares went below $10.

- On Wednesday, the stock dropped 25% on news that Enron was unable to line up $2 billion from private investors.

On Friday, Enron announced the merger with Dynegy. Shares rose 16% to $10.

On Tuesday, November 13, $2 billion arrived for Enron. They took a breath, but it wasn’t enough.

- Enron realized it was going to need to repay more than $9 billion by the end of 2002. It would need a lot more money.

- Enron’s trading partners continued demanding collateral. The number of transactions plummeted, and trading profits crashed.

- An SPE (Rawhide) was structured to unwind if its debt had been downgraded to one step above junk. It now had to repay $690 million in debt.

- In six days, Enron had burned through a billion dollars. Its stock fell to below $5.

On Dynegy’s side, the lack of transparent disclosure of possible problems and Ken Lay’s insistence on maintaining control of Enron crashed the deal. The banks weren’t coming up with more money that Enron needed.

On Wednesday November 28, the rating agencies cut Enron into junk territory.

- This triggered $3.9 billion in debt.

- Dynegy officially canceled the deal.

- Enron Online shut down. Shares dropped to $0.61

Banks moved to minimize their losses, asking for return of collateral. Enron didn’t have it.

On Sunday, December 2, Enron filed for bankruptcy.

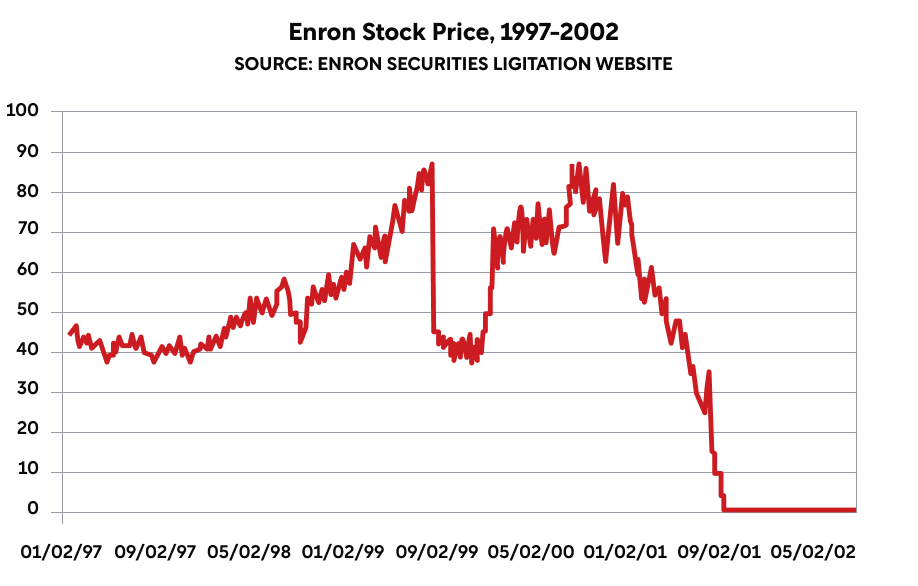

Here is Enron’s complete stock price history:

The Legal Aftermath and Enron's Legacy

As the largest bankruptcy in US history to that point, the public demanded heads. And there were many responsible parties to punish.

The clearly illegal smoking guns led to straightforward convictions - Fastow’s misrepresentations about LJM; asset sales that were booked as revenue but in reality had a guarantee to be rebought, which meant it was a loan.

Arthur Andersen, previously one of the big five accounting firms, was convicted of obstruction of justice in 2002 for shredding documents. It voluntarily surrendered its licenses to practice as CPAs in 2002.

- (The Supreme Court later reversed the conviction in 2005, though by that point its besmirched reputation prevented it from gaining any clients.)

The banks agreed to write big settlement checks, ultimately producing $7.2 billion for shareholders (about 20 cents for each dollar lost).

Beyond these, the legal difficulty was that most of the financial maneuvers were not technically illegal (which is why Fastow so brazenly boasted about the structures, and Wall Street praised them).

There also was no smoking gun that indicated either Lay or Skilling knew the extent of risk taken and predicted Enron’s demise. On deal forms, many signature lines for Skilling were left blank. They blamed Arthur Andersen and their lawyers for not detecting problems.

- For years, Lay and Skilling maintained that what they did was no different from the overoptimistic projections by dotcom companies. Instead, they had always been targeted unfairly by short sellers.

Ultimately, prosecutors chose a simpler, broader strategy - rather than analyze specific transactions and prove their illegality, they asserted that Enron had severely misrepresented Enron’s financial health, manipulating public earnings through devices designed to produce misleading results and failing to disclose facts about Enron’s dire position.

- Examples of things that should have been disclosed - EES losses being hidden in wholesale; writedowns in bad deals like Azurix; meltdown in SPEs like the Raptors; last-minute filling holes to make quarterly financials look better.

- Furthermore, accounting rules barred a company from using its stock to boost its income statement.

- Other things that looked bad in trial - their cashing out of lots of personal shares; extravagant lifestyles; legal settlements with many Enron employees (if nothing was wrong, why had they all settled?)

In May 2006, the jury found Skilling and Lay guilty. Lay died in July from a heart attack (some suspected he faked his death). Skilling was sentenced to 24 years in prison and a fine of $45 million.

The massive failure of Enron also spurred regulatory changes:

- Sarbanes-Oxley increased the personal liability of CEOs for financial statements; instituted requirements for auditor independence; and increased penalties for securities fraud.

- The Credit Rating Agency Reform Act aimed to reduce lack of competition between the big three agencies. (This didn’t kick in strongly enough in time to prevent the subprime mortgage crisis in 2008.)

History Repeats Itself

In the afterword, the author connects the Enron scandal to the 2008 crisis. There were many similarities between the two:

- Multiple stakeholders looked away while they got rich. This even includes the public, which could buy houses more easily than ever before.

- After the crisis, more regulation was passed, with the promise that now everything would be different.

Differences between Enron and 2008:

- The author believes Enron was genuinely trying to be innovative. It launched new business lines (online energy trading, video on demand, international development).

- In contrast, the banks in 2008 were merely issuing loans to people who couldn’t pay them, repackaging bad loans and misrepresenting their worth.

- There could have been a case where Enron worked out; there was never an option for the latter.

- There were no prosecutions of major bank executives.

It seems, therefore, that we haven’t really learned our lessons, and the future won’t be any different. People will be greedy; there will always be blurry lines around what’s technically legal but immoral. It’s human nature.

Enabling Conditions of Enrons Deception

How was Enron able to get away with its bad behavior for so long, even when its operations involved thousands of people with partial insight into the problems? Here we take a look at the major conditions that promoted Enron’s deception. These are themes that might recur in future disasters.

(Shortform note: while the original book mostly tells a chronological story, we pulled the themes and patterns from the book to form this chapter.)

People with Incentives to Tolerate Bad Behavior

People who could have stepped in and intervened didn’t, often because they had a large personal stake in Enron’s success. Further, the more Enron became a success (like in terms of stock price or deal flow), the more beholden the stakeholders were to Enron.

Furthermore, everyone looked to each other for validation. “Surely all these other people can’t be wrong!” Yet no one realized no one else had done their due diligence.

In a culture where earnings are prized above all, earners have the leverage to conduct bad behavior, unpunished. Threaten to quit and you get what you want. This culture promotes caring about self rather than the longevity of the company.

- In the 1980s, an Enron oil trader ignored trading limits and siphoned money to himself. This was overlooked by management since his department was a golden goose. Letter from Enron management to trader: “I have complete confidence...please keep making us millions.” (He eventually had a disastrous short position that could have bankrupted the company.)

Breaking down each of the stakeholders:

Employees

- Employees who had an inkling something was wrong were willing to look the other way for big compensation and a rising stock price. Why would you want the music to stop when you’re planning on buying a vacation home?

- The market seemed to justify what the business was doing - surely professional investors with billions at stake couldn’t be wrong?

- Furthermore, skeptics within the company were publicly punished by being reassigned. For many, the risk of being punished wasn’t worth the gain from exposing wrongdoing.

Public markets

- In a period of dotcom bullishness, the possibilities were uncapped. All sorts of companies with illusory projections were propped up.

- Investors tolerated Enron’s opacity, since the stock was up and to the right.

- Investors circulated a mythos of Enron being an untouchable, invincible company.

Consultants/accountants

- Arthur Andersen’s consulting had Enron as one of their biggest customers (paying $52MM in 2000). Enron kept competitors closeby to threaten Arthur Andersen into validating their deals.

- AA staff who grew Enron fees were promoted. Further, Enron hired dozens of Andersen accountants, giving individuals pressure to be seen by Enron as a team player.

Bankers

- Banks earned large fees from Enron’s complicated structured-finance deals ($240 million in 1999), and bankers who grew deal sizes got promotions.

- Like with accountants, Enron kept multiple banks in the wings competing for its business.

- Banks even tolerated Andy Fastow’s self-dealings with his private funds, because he was the gatekeeper between banks and Enron deals.

Outside analysts

- Putatively, the analysts issuing buy/sell recommendations should be separate from the investment banking arm of the same bank. In reality, they were closely tied - companies would only give deals to banks who issued a buy recommendation with aggressive price targets.

- In the 2000 era, buy/sell recommendations could move stock prices, so company shareholders resented sell recommendations, however well-reasoned.

- So analysts focused on earnings-per-share estimates to the exclusion of cash and debt.

- Analysts even competed with each other for higher price targets - $100, $115.

- At least one analyst who was skeptical of Enron was pressured to be fired by Fastow.

Ratings agencies

- Moody’s and S&P should have issued downgrades for the sake of protecting their reputation. They had massive leverage over Enron, since their rating could sink Enron. Why didn’t they dig deeper?

- For one, Enron simply stated they needed sufficiently high ratings to keep getting debt - lowering ratings would force debt paybacks and cause a selloff, which would sink the company. The ratings agencies didn’t want to be single-handedly responsible for sinking a company, just in case they were wrong.

- Further, even ratings agents may have held stock in the public markets and were caught up in the flurry.

Believable Guiding Visions

As a company, Enron saw itself as a modernizer of ancient industries. They were all doing “the Lord’s work” and “spreading the privatization gospel.”

- Members of Enron’s trading department were missionaries - they saw themselves as revitalizing an industry populated by dinosaurs and bringing efficiency through free markets.

- Enron international developers saw themselves bringing efficient privatized energy to poor countries.

- Andy Fastow’s department saw themselves as financial wizards, pushing the boundary of what could be achieved in finance while staying in the bounds of GAAP accounting. They were just playing the rules of the game. They also saw themselves as saviors in the company, filling the holes that other departments created and providing real P&L value to Enron.

Gradually as workers become corrupted, they can justify their actions in terms of the original vision.

Poorly Constructed Compensation Schemes

A pattern of Enron’s compensation style was to reward short-term behaviors (like stock price or closing deal sizes) without concern for long-term value (like profitability). And according to the book’s author, Skilling happily fed greed, believing it was the best motivator for performance.

Deal makers were compensated by future expected cash flows when the deal closed, not on the generation of actual cashflow. So deal makers hungrily moved from one deal to another, leaving the actual execution and capture of cashflow aside.

- This was originally done to avoid giving direct equity in projects to developers.

- “If you’re told to make $25 million and you do it, you’re in great shape. It doesn’t matter how much it costs you to make that $25 million.”

- This happened in the international development deals under Rebecca Mark, and in EES under Skilling.

- The projections of future profits included wildly optimistic price curves at the end.

- Perspective of salespeople: “I’m not going to be around 5 years from now - why should I care whether this deal works?”

Employees had incentives around short-term stock prices.

- In early 1990s, options for Lay and Kinder vested earlier if it showed 15% annual growth each year.

- At one point, employees were promised twice their annual salary in Enron shares if they met annual share price performance targets. This of course encouraged manipulation of stock price above fundamentals

- This made employees desperate to hit earnings targets before the quarter closed, prompting bad deals and aggravating future problems.

- Skilling wanted to avoid downgrades of Enron’s stock, knowing that losing confidence once would make it hard to regain.

- The stock ticker was everywhere in Enron offices - in the lobbies, on computer screens. Dips in stock price caused dips in morale.

Peer performance reviews made big differences in bonuses, and allowed politicking - originators bullied risk department employees into approving bad deals; angry managers would dig in their heels for their staff to get top rankings.

Accounting Practices that Disguised the Fundamentals

As explained throughout, Enron’s aggressive accounting stretched the limits of allowable practices, allowing it to inflate revenue while hiding losses.

Mark-to-market accounting allowed declaration profits of long-term contracts instantaneously.

- The subjectivity of those future prices could heavily distort the profits before any cashflow occurred.

- This led to rapid initial growth with large paper numbers, but required additional deals to show continuous growth each quarter (since the entire deal had already been accounted for in the previous quarter).

- Long-term contracts could be reworked to post additional earnings, akin to double-dipping.

- In the lifetime of the deal, if Enron suspected a deal would end in losses, they should have been reported on the balance sheet and profits - but sometimes they didn’t.

- Philosophically, Skilling insisted that the value of the deal was in the idea, and once the idea was executed it should be rewarded. Future people shouldn’t be rewarded for the actions of people in the past.

For its trading, Enron used the aggressive interpretation of recognized the selling price of goods as revenue, rather than merely the trading fees.

For lost projects, instead of writing them off as a loss, Enron would book costs as an asset, which came to be known as a “snowball.”

Dead deals were fictitiously kept alive, to avoid a writedown that quarter.

Complicated SPE deals gave off-book debt

- In summary, they allowed Enron to hide debt from its balance sheet, book loans as revenue, hide losses, and overstate its equity.

- Enron suggested it used SPEs to hedge against downside risk for its illiquid investments. In reality, the SPEs were using Enron’s stock as guarantees, thus not producing a hedge at all.

- See the SPEs/minority interest transactions/prepay section above in Enron’s History.

Nonrecurring revenue was presented as part of ongoing operations - reworking of supply contracts, selling stakes in its facilities.

In 1997, Enron began using “Total Contract Value” as a pseudo-metric of growth, similar to the dot-com metrics of “eyeballs” and “hits.” In reality Enron could be losing money on every deal.

Poor Management Appointments

Enron was characterized by the wrong people in the wrong positions of power.

At the highest level of management, weak managers with the wrong intentions were placed into power.

- The aggressive Skilling was promoted to COO, instead of the more realistic Kinder as CEO.

- Andy Fastow was promoted to CFO, even though his experience was in creating financial structures, not in financial prudence.

- Ken Lay was more interested in being a public figure than managing business

- He was celebrated as a business sage, leading an old industry into a new era.

- Lay was also a weak manager, wanting others to like him and avoiding tough decisions.

- A weak board

- Ken Lay filled the board with people who had reciprocal relationships with Enron - a consulting contract, phantom equity, donation to a hospital.

- Ken Lay appeared to walk on water. He seemed indispensable and everything great about Enron seemed to be attributable to him.

- The risk department was underpowered, led by a meek person who didn’t push back against bad deals

Throughout the company, Enron generally promoted people with the wrong kind of ambition (centered on self rather than the company’s long-term success).

Businesses that Simply Didn’t Work

Enron habitually launched big into new markets, spending extravagantly in the belief that they would make it back many fold. Skilling believed worrying about cost stifled creativity.

Enron’s/Skilling’s optimistic promises to Wall Street created a situation where Enron had to deliver fast on businesses, or else their stock price would plummet.

Overall, Enron’s businesses lost over $10 billion in cash over their life.

Of course, the failed businesses exacerbated the situation - to hide the losses, they relied on increasingly complicated and questionable deals.

- Enron desperately needed to produce earnings to avoid violating its loan agreements. Further, because of its low cash, it needed new loans to pay back maturing loans.

- Enron couldn’t put too much debt on its balance sheet, which would hurt its credit rating, and banks would stop lending.

Drinking their Own Kool-aid

Executives loved the misguided impression given by press.

- Rebecca Mark for being a female phenom dealmaker

- Skilling for Enron being the golden child of the old energy industry

- Lay for being the prophet philosopher who saw the deregulation happening

- Enron in general for being the new age energy company with exciting new business line

Wall Street loved Enron’s setup of the Risk Control Committee, believing it would allow Enron to take on more risk safely. This impression likely helped Enron execs and board overestimate its contribution.

In the late 1990s, companies had to move at Internet speed to keep up with other companies. Enron wanted to be seen as more like dot-coms than like Exxon.

Enron’s finance teams established a reputation as financial wizards, stretching the rules to create a new paradigm of practice. Lehman Brothers on Fastow: “He has invented a groundbreaking strategy.” Bankers saw working with Enron as a badge of honor.

- This allowed Fastow to justify participating in his own deals as the 3% outside capital in an SPE.

No one seemed to confront the possibility that Enron stock might actually fall.

Personal Traits of Enron Managers

Much is written about the management styles of the senior executives at Enron. They each had idiosyncracies that, when combined, led to a proliferation of problems.

Jeff Skilling, COO then CEO

- An intellectual purist, a designer of ditches, not a digger of ditches. Often slow to recognize when reality didn’t match theory. Left the execution details to his lieutenants.

- “I’m not particularly interested in the balance sheet. It seemed to be doing well. We always had money.”

- In the retail Enron Energy Services business, Skilling disparaged the operators of utilities as “buttcrack “ workers. “This stuff sells. Now we have to actually do something for the customers. That’s the easy part.”

- A gambler at heart, always assumed he could beat the odds. (He was wiped out in the stock market twice in his teens.)

- Convinced he was the smartest guy in the room - anyone who disagreed wasn’t smart enough to get it

- He bullied analysts who questioned how Enron made money. If he didn’t want to answer a question, he dumped a lot of data. If you still didn’t get it, he’d call you stupid.

- Darwinian in management. Encouraged confrontation between subordinates.

- When developing a business, price was no object - the business Enron could build with an asset would far outweigh a higher price in the beginning.

- Rarely pushed back on deals he believed were bad, promising to hold people accountable but rarely doing so.

- Obsessed with Enron’s stock price on a daily basis.

Ken Lay

- Loved his public persona as a business sage, leading an old industry into a new era

- Became engrossed by his charity foundation, networking with Washington elite, and being a local gatekeeper in Houston politics. Aimed to be treasury secretary.

- Known internally in Enron as a pushover when negotiating pay and bonuses.

- Was a weak manager, wanting others to like him and hiding behind the board for tough decisions (like not promoting Rich Kinder). Lied to keep people from getting mad at him

- Wall Street analysts viewed him as useless and out of touch with how the business worked - they preferred Kinder who delivered the numbers.

- Used Enron’s resources for his family (family use of company jets) and engaged in nepotism (used a relative’s travel agency to book Enron flights).

- Became a missionary for deregulation

- This had worked once before in natural gas.

- He inappropriately applied this mission to retail utilities, without proof that the states were actually moving in this direction. Enron bet big and lost.

Andy Fastow, CFO

- Burned with ambition, “not necessarily to be the best but to be seen as the best”

- Exaggerated his resume to claim greater credit for securitization work

- Had a chip on his shoulder by being in finance and not a department with P&L. Wanted to establish finance as a profit driver and thus sharing in the bonuses

- A gratuitous self-promoter and brown-noser

- Had a short temper, causing people to be afraid of speaking out

Shortform Exclusive: How to Avoid an Enron

Here we invert the question - how do you avoid building an Enron? Make sure you avoid the bad practices of Enron with this checklist.

- Don’t tolerate bad behavior just because they’re making money for you.

- Don’t avoid doing diligence because you believe that everyone else has done their due diligence. Everyone else likely believes the same, and it’s possible no one has done diligence.

- Do sanity checks even if you fear being called dumb. Lose your ego around being intelligent - if something seems too complicated for you to understand, it’s probably not because you’re dumb. Someone might be actively hiding something.

- Set compensation schemes correctly - in service of long-term value and sustainability, not in terms of misleading short-term metrics.

- Avoid these standard excuses that are more reassuring than they should be.

- “It’s fine to be over-optimistic in our estimates - analysts don’t have to believe it.”

- “The proper controls are in place. I could be removed at any time if I were doing something wrong. The company doesn’t have to do any of these deals - they can reject them at any time.”

- “This will have no impact on our earnings/statements.”

- Don’t let management lose sight of the fundamental nature of business and relax their oversight.

- Avoid too-clever schemes that stretch the rules for the promise of a quick return.

- Don’t overlook seemingly small things like compensation - even small percentage incentives can contribute to the problem. Don’t be sloppier than you need to be, just because small terms don’t seem to matter.

- Don’t believe what the press writes about you (both positive and negative). They see so little of the situation that they’re often not reliable.

- Don’t use superficial markers of progress (deals on paper, valuation of deal) instead of real fundamental progress (cashflow).

- In good heady times, don’t lose grasp on the discipline that got you there. This is when you get overconfident and make bad bets.

- Don’t wait to bite the bullet on bad news. Avoid hoping for a bet-it-all strategy that will pay off and rescue the company.

- Be careful doubling down on a key assumption that, if falsified, would cripple everything. In Enron’s case, they believed their stock price would never fall, allowing them to use Enron stock to prop up shaky deals.

- Don’t avoid taking seriously the concerns of employees on the ground. Be careful of dismissing them as not seeing the bigger picture.

- When the financial grim reaper comes, clamp down spending and appearances immediately. Don’t fly on private jets.