1-Page Summary

The premise: when growing up, author Robert Kiyosaki had two dads advising him: 1) a Stanford-educated PhD who followed traditional career thinking, was allergic to risk, and was financially illiterate (the Poor Dad, his biological father); 2) a high school dropout who later built a business empire worth many millions and employing thousands (the Rich Dad, his best friend’s father).

The Poor Dad represents the traditional view on work and money - go to school, get a good job and climb the ladder, prize stability over independence, buy a house, and spend money without a clear long-term plan.

- Most parents belong to this system, so they pass it down to their kids.

- The traditional view worked better in the 20th century, when strong growth and decades-long employment meant stability was a viable strategy. Nowadays, pensions are rarely guaranteed; job security at a loyal employer is rare; professional education and academic success are no longer guarantees for security.

The Rich Dad represents what was then a more contrarian view - work for salary if you have to, but aim for financial independence; have your money generate more money; and take calculated risks boldly.

Most people adopt the Poor Dad view of finances and life. Even worse, they let money control their life:

- Fear of not having money makes people work hard.

- Then once they get a paycheck, greed gets them to buy things they covet.

- But the joy is short-lived. As they spend unwisely, they have money problems, and the fear of not having money drives back in. They have to go back to work to get the next paycheck.

- This cycles endlessly, even as their paychecks increase with raises - this is the Rat Race. Money ends up running their lives. They get stuck in jobs they dislike for the sake of money.

Lesson 1: The Rich Don’t Work For Money - Money Works for Them

The rich don’t get rich merely by being paid higher salaries (though this is a great help). They get rich by owning things that make them more money.

Wealthy people use their Income to buy Assets that return more Income. Meanwhile, they minimize their spending on Expenses and buying Liabilities, to have more money to buy more Assets.

People who don’t become rich either spend all their income on expenses, or buy liabilities that increase their expenses but don’t add income.

The key to financial independence is having money that makes more money. You want your money to make enough money that you don’t have to work anymore.

Lesson 2: Buy Assets, Not Liabilities

The key is to buy things that generate income (assets). You do NOT want to buy things that lose money over time or incur large expenses (liabilities).

This is obvious enough. But the most deceptive investments look like assets, but are actually liabilities.

- Example: buying a house as your primary investment. This viewpoint is problematic because it gets people to buy more house than they really need. A more costly house vacuums up money with high monthly expenses - money that could have been put more profitably elsewhere.

Real assets are businesses that don’t require your active management; stocks, bonds, and other securities; income-generating real estate; and intellectual property generating royalties.

Think about each dollar as your employee that works 24 hours a day tirelessly to make you more money.

The tradeoff between today’s expenses and future income should be clear. Every dollar you spend today is a dollar that does not work for you again, in perpetuity.

Lesson 3: Reduce Taxes through Corporations

Kiyosaki advises that people set up corporations to deduct expenses without paying taxes. (Shortform note: This is a controversial suggestion because it can easily go wrong if you don’t follow tax guidelines.)

The major thing worth noting here is that corporations let you deduct legitimate business expenses pre-tax, instead of paying from post-tax dollars.

Lesson 4: Overcome Your Mental Obstacles

Even if you have Rich Dad goals, you still need to execute your plan. Several common mental obstacles get in the way. We’ll address each one:

Self-doubt

- In the real world, more than just intelligence and grades is required. Guts, chutzpah, balls, daring, tenacity, grit are different names for the factor that plays a huge role in success.

- When you recognize a great opportunity, you must have the courage to chase it.

Fear

- Fear of losing makes you play it safe and avoid opportunities that can have huge upsides and relatively low downsides.

- Remember that failure will only make you stronger and smarter. Use your failure to inspire yourself to become a winner. Use this thinking to lower the perceived cost of failing.

- Fear of ostracism prevents people from having nonconsensus opinions. As it relates to finance, it’s in 1) not bucking the consensus traditional way of handling your career and money, 2) keeping up with the Joneses and matching their irresponsible spending. Focus on yourself and your personal goals, regardless of what other people think.

Laziness

- Counterintuitively, busy people are often the most lazy. They stay busy as a way of avoiding something they don’t want to face.

- Consider someone who’s moving all the time and brushes off investment opportunities as, “I’m working hard enough as it is, and my boss wants me to do more work. I don’t have the time.”

Guilt for Feeling Greedy

- Condemning greed might be a trained defense, learned helplessness. “I don’t know how to become rich. So I’m just going to try to believe being rich is bad, and there’s valor in not wanting to be rich. Even though secretly I would love to be rich.” It’s easy to imagine parents feeling this, then teaching it to their kids.

- Instead, embrace your greed. Money is empowering, and you have the right to design the future life that will make you happiest.

Arrogance

- When you’re ignorant in a subject, recognize this, then educate yourself.

- Intelligent people welcome new ideas, since new ideas add synergy with other ideas.

- Don’t feel a trade is underneath you. Some people have an allergy to learning sales techniques, without realizing that much of the world runs on sales of some sort.

Lesson 5: Develop Financial Intelligence. Keep Learning

Financial intelligence consists of knowledge in accounting, investing, markets, and law.

Financial intelligence allows you to construct creative ways to solve financial problems, vet the ones that are more likely to work, then have the technical ability to execute them.

Knowledge compounds in a scary way. Making yourself 1% better each day will pay off huge returns compared to someone who stays static. And the faster you can iterate your knowledge, the faster the returns compound.

Shortform Introduction

Rich Dad, Poor Dad is one of the best-selling financial books in history, selling over 35 million copies since its publication in 1997.

The book doesn’t teach the tactics of getting rich as much as it does the principles: the mindset and high-level strategies that distinguish the wealthy from the hapless.

Unfortunately, as many critics have commented, much of Rich Dad, Poor Dad is flawed. It’s not clear exactly how and when to apply the principles, and less discerning readers can follow the advice and get into trouble. Here are some caveats to set the advice in context.

Rich Dad, Poor Dad doesn’t engage on tactical details that would help people apply the decisions. Kiyosaki says these are out of scope of the book, and maybe details would alienate the popular reader, but it’s a poor excuse. Examples of useful questions to cover:

- When does it make sense to rent vs buy a house? What will end up being a better financial decision in the long run?

- How do you assess the risk and return of an investment? How do you compare different investment opportunities to each other?

- What do the data show on how higher education affects one’s income?

Kiyosaki includes pretty outlandish examples of fantastic investment opportunities. These aren’t necessary for understanding the principles (and we omit most of them from this summary), but they are misleading for the more gullible reader. Here they are, for your understanding:

- He mentions foreclosed houses worth $75k that he bought at $20k and flipped for $60k within 5 hours of work.

- He mentions turning an investment on the order of $5,000 into a million dollars while waving away the details.

- In the most optimistic case, these were cherry-picked, best-case-scenario examples. In a pessimistic case, they were fabrications.

Rich Dad, Poor Dad has some advice that can be interpreted irresponsibly and lead to disaster.

- Robert Kiyosaki advises people to start their own corporations and pay for expenses pre-tax. He implies that they should be legitimate business expenses, but doesn’t clearly define this. A novice can get easily

- He likes the Texan attitude: “if you’re going to broke, go big.” This can provoke disproportionate risk-taking for the uninformed.

- Even if people follow his He always has plausible deniability with, “it’s not my fault you didn’t learn more and make better decisions.”

Robert Kiyosaki seems to lean toward the libertarian. He has standard anti-taxation, anti-entitlement, pro-gold-standard party lines.

- For example: “The real world is simply waiting for you to get rich. Only a person’s doubts keep them poor.”

Again, despite its flaws, the book has useful things to say. So try to focus on the principles we’ve extracted and what you can take away.

Finally, Rich Dad, Poor Dad is obviously a book about making more money. Most people, whether they admit it or not, would like more money. More money can mean more available options, greater freedom, and less stress. One can also desire money without thinking that all happiness comes from money. If you don’t agree with any of this, that’s fine.

Introduction: Rich Dad and Poor Dad

Growing up in Hawaii in the 1950s, Robert Kiyosaki had two dads:

- Poor Dad: His biological dad, who was well educated (Stanford grad, PhD from Northwestern) but had the traditional mindset: work hard, get a stable job, and be financially conservative. The family did fine, but never made it to financial independence and left little to their kids.

- Rich Dad: His friend Mike’s dad, who didn’t graduate from high school and had his own financial ups and downs, but eventually built a local business empire and employed thousands. (believed to be Richard Kimi)

Robert Kiyosaki got conflicting advice from both dads on how to manage money, career, and financial risk. Ultimately he saw more wisdom and results in Rich Dad’s advice, and followed in the Rich Dad’s path.

While Robert Kiyosaki might really have had two dads, the more important point is that the two dads are a parable for two types of financial thinking.

- The Poor Dad represents the standard consensus view on work and money - go to school, get a good job and climb the ladder, prize stability over independence, buy a house, and spend money without a clear long-term plan.

- The traditional schooling system trains this style of thinking. (Plus, employers have the incentive to keep workers thinking this).

- Most parents belong to this system, so they pass it down to their kids.

- The Rich Dad represents what was then a more contrarian view - work for salary if you have to, but aim for financial independence; have your money generate more money; and take calculated risks boldly.

The traditional view worked better in the 20th century, when strong growth and decades-long employment meant stability was a viable strategy. Nowadays, pensions are rarely guaranteed; job security at a loyal employer is rare; professional education and academic success are no longer guarantees for security.

But the traditional thinking is still common. Rich Dad, Poor Dad aims to shake readers out of their current passive path and taking a proactive strategy to building wealth and working for their best interest. Figure out what to do with money once you earn it, learn how to keep people from taking it from you, and make the money work for you.

Rich Dad, Poor Dad explores differences between the two dads on a few levels:

- Mindset: how responsible each felt for financial literacy and proactively making good financial decisions

- Strategy: how they allocated their income among assets and liabilities, how they perceived risk

- Tactics: how they set up their income to lower taxes, what investments they make

What Rich Dad and Poor Dad Say

Rich Dad and Poor Dad look at the world differently. Here are quotes and perspectives taken from throughout Rich Dad, Poor Dad that exemplify their different mindsets and approaches to wealth.

| Poor Dad | Rich Dad |

| Be employed by a company. Climb up the corporate ladder. | Own the company. Own the corporate ladder. |

| Be a smart person. | Hire smart people. |

| I can’t afford it. (passive surrender) | How can I afford it? (active engagement) |

| The reason we’re not rich is because of you kids. (blaming others for lack of wealth) | The reason I must be rich is because I have you kids. |

| Play it safe. Don’t take financial risks. | Risk is good when controlled. Learn to manage risk. |

| Our home is our largest investment and our greatest asset. | Our home is a liability and shouldn’t be our largest investment. |

| Find a good job. | Create jobs. |

| Work for money. | Money works for me. |

| Security is most important. | Learning is most important. |

| I’ll never be rich, no matter what I do. | No matter how much money I have, I am always a rich man. There’s a difference between being broke and being poor - broke is a temporary state; poor is a permanent mindset. |

| Money doesn’t matter. (This is often self-deception to avoid confronting the pain of not having enough money.) | Money is power. Money does matter, whether you like it or not. Learn how money works, and you gain power over it. |

| Greed is bad. | Use greed to make your life and other people’s lives better. |

| I’ve worked hard, and I’m entitled to benefits. | Be self-reliant. Entitlements are weakening and cause financial dependence. |

| The fear of losing is greater than the excitement of winning. Play it safe. (Die a boring person, knowing you didn’t go for it.) | Control your fear. Don’t let it make you a slave to money. |

| More money will solve my problems. I’m in debt. How do I make more money? | For most people, lack of financial education is the major problem. If you give people more money without changing their financial strategy, the money will just disappear.

The problem is how to spend the money you do get. Rework the cashflow pattern first before getting more money. |

| I need more money, so I’m going to get a job/get a promotion/go back to school and get a raise/get a second job. | Let’s think carefully. Is a job the best solution to this over the long run? How do I make income beyond just earning a higher salary? |

| (To another person) Congratulations! You got a good job with a solid employer. | A job isn’t as great as you think it is. Who are you selling your time to? Who are you making rich? |

| Borrow money to get what you want. | Focus on creating money first. Then buy things with the excess money that your money generates. |

Learning with Rich Dad

Spread across a few chapters in Rich Dad, Poor Dad, the author narrates his experience with Rich Dad learning the principles of money and work.

Learning the First Lesson

As a 9 year old, Robert Kiyosaki is rejected socially by the rich kids in his public school. He asks his dad, a teacher, how to get rich and make money, but his dad has no satisfactory answer.

He commiserates with his best friend Mike, the only other non-visibly-wealthy kid in the school. They start a misguided idea to melt down metal toothpaste tubes and mint their own nickels. Bemused, Robert’s dad (Poor Dad) suggests they talk to Mike’s dad (Rich Dad), who owns multiple local businesses and seems to be on a good path.

- Poor Dad also notes that the other apparently rich kids have parents who are just like him - they’re employed by the local plantation, and if the company gets into trouble, they’ll soon have nothing. Rich Dad is different since he seems to be paving his own way.

Rich Dad is busy, but meets with them early in the morning between his regular business meetings with his managers. Rich Dad has this dialogue:

- “Here’s my offer. I’ll teach you, but not like a teacher in a classroom. Work for me, and I’ll teach you. Don’t work for me, and I won’t teach you. You’ll learn faster if you work. That’s my offer. Take it or leave it.”

- “Can I ask a question first?” Kiyosaki asks.

- “No. Take it or leave it. I’m too busy to waste my time. If you can’t be decisive and make up your mind quickly, you’ll never learn to make money. Opportunities come quickly and go quickly. You need to know when to make fast decisions. I just gave you an opportunity that you asked for. Will you take it?”

They take the deal, which means working for 10 cents an hour in Rich Dad’s convenience store. They know this is an unfair wage.

After laboring for 3 hours over 3 weekends, Robert Kiyosaki gets upset and wants to quit. His friend is amused, since Rich Dad expected he’d want to quit, and wanted to meet afterward.

Before the meeting, Poor Dad advises the author to demand what he deserved - at least 25 cents an hour. If he doesn’t get the raise, Poor Dad counsels, Robert Kiyosaki should quit immediately.

Kiyosaki takes Poor Dad’s advice, and starts the meeting demanding more money, demanding to be treated better, threatening child labor lawsuits, and complaining the Rich Dad hasn’t taught him anything. Rich Dad replies: “Not bad. In less than a month, you sound like most of my employees.”

Rich Dad’s point of the exercise is this:

- Most people accept jobs with lower pay than they deserve out of fear - fear of not paying their bills, of being fired, of not having enough money, of starting over. Fear governs their emotions around money, and they become a slave to working to make money.

- Life pushes everyone around. Many people quit and let the pushing happen. Some get angry and push back, but in the wrong direction - against the boss, their job, their spouse, or the world. Others learn the lesson, try to get better, and move on.

- By getting angry, the author showed Rich Dad that he had enough passion and independence of mind to be worth teaching.

Rich Dad is pleased and says, “you boys are the first to come to me asking how to make money. Over 150 employees work in my companies, and not a single one has come to me to learn about money. They ask for a job or a bigger paycheck, but never to educate themselves about money. So they’ll spend their lives working for money, but not actually understanding it.”

Working for No Pay

Rich Dad’s next order is for the author and Mike to go back working, but now with zero pay. When Kiyosaki complains, Rich Dad challenges him: we can go back to our original deal of 10 cents, or you can do what most people do - complain there isn’t enough pay, and go looking for another job. When Kiyosaki is confused, Rich Dad advises him to use his head.

After working for 3 more weeks, both kids are confused by what they’re supposed to be learning. Rich Dad comes by and tells them there’s a lesson to be learned here.

“If you don’t learn this lesson, you’ll end up like other people who work hard, clinging to their pay and constantly looking forward for their vacation days and little raises. Here - I’ll raise your pay to 25 cents an hour. Does that excite you? Do you want to take it?”

Rich Dad keeps raising the stakes - a dollar an hour. $2 an hour. The author’s imagination runs wild at having that much money, but he knows he’s being tested. Each person has a weak and needy part of their soul that can be bought. Each person also has a part of their soul that is strong and can never be bought.

The point of the lesson: most people run endlessly in a loop between fear and greed.

- Fear of not having money makes people work hard.

- Then once they get a paycheck, greed gets them salivating over all the things money can buy. They spend the money thinking it can buy joy, but the joy is short-lived. Soon they have money problems, and fear drives back in.

- This cycles endlessly, even as their paycheck increases - this is the Rat Race. Money ends up running their lives.

- Even rich people are subject to this fear - the more money they get, the more terrified they are of losing it. They fear losing social standing, and the weak part of their soul gets even more desperate.

Rich Dad was trying to teach the kids not to give into emotions around money, but rather to delay reactions and think.

- Taking on the job for free was the first resistance to emotions.

- Next, raising the hourly wage for the kids was a metaphor for adult salaries. Incremental raises trigger hopes for incremental advancements to life, causing people to live in a perpetual loop and never truly exploring their dreams.

The Breakthrough

Rich Dad leaves with this advice: “The sooner you stop thinking you need a paycheck, the easier your adult life will be. Keep learning, keep using your brain, keep working for free, and your mind will make you more money far beyond what I could afford to pay you. You will see opportunities right under your nose that other people choose not to see. They’re blind to these opportunities because they look anxiously for money and security.”

After a few more weeks of working for free, one day Kiyosaki has an insight - the store he worked in regularly disposed of its comic books. Could they collect the books, then start a comic book library open to the public? They could charge other kids 10 cents admission for unlimited reading - a clear bargain, since a comic costs 10 cents each.

After some work, they launch with great success. They earn $9 per week over 3 months. They pay Mike’s sister $1 a week for managing the store.

After three months, bullies break into the room, and Rich Dad suggest they shut down the business. But the lesson was learned: by not being paid, they were forced to find opportunities to make money. They avoided being distracted by the short-term carrot.

Lesson 1: The Rich Don’t Work For Money - Money Works for Them

With the narrative over, the rest of the book covers Robert Kiyosaki’s major lessons from Rich Dad.

Most people work 40+ hours a week to earn salaries. Many then take their earnings to 1) buy stuff they think will make them happy (but this is short-lived), 2) save the remainder in a conservative way.

While this ensures some degree of stability, it doesn’t make you rich. And working to earn a pension makes you financially dependent - let alone the risk that pensions won’t be funded decades from now, when you need it.

The counter-intuitive lesson here is this: the rich don’t get rich merely by being paid higher salaries (though this is a great help). They get rich so by owning things. No one on the Forbes billionaire list got there purely with a salary.

(As tech investor Sam Altman says, “You get truly rich by owning things that increase rapidly in value. This can be a piece of a business, real estate, natural resource, intellectual property, or other similar things. But somehow or other, you need to own equity in something, instead of just selling your time. Time only scales linearly.”)

When you work for an employer, you get paid only a fraction of the value that you generate for the employer (otherwise, if the business would go bankrupt). Say your salary is $50k a year. Your work may allow your employer to earn $100k in sales that year, yielding a clean profit after deducting your salary.

- Even further, if your work isn’t just a pure service but also builds value in the company - say in R&D or product improvement - the value may be many multiples of your salary.

The key to financial independence is having money that makes more money. You want your money to make enough money that you don’t have to work anymore.

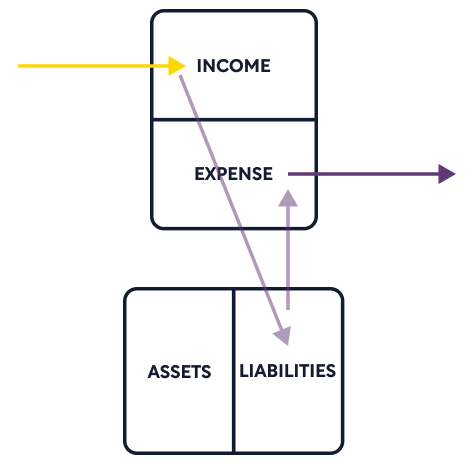

Cashflow Diagrams

To picture this, here’s a simple financial diagram from Rich Dad, Poor Dad on how cashflow and balance sheet relate to each other:

The top box is an income statement, measuring how much income you get in a period, and how much expenses you pay out.

The bottom diagram is the balance sheet. It shows how much in assets and liabilities you have. Assets are things that make money over time. Liabilities are something that spend money over time. (Shortform note: these are Robert Kiyosaki’s terms and don’t follow typical GAAP accounting.)

We’ll get more into distinguishing assets vs liabilities in the next section, but the main point here is that wealthy people use their Income to buy Assets that return more Income. Meanwhile, they minimize their spending on Expenses and buying Liabilities, to have more money to buy more Assets. Here’s what that looks like:

People who don’t become rich either spend all their income on expenses, or buy liabilities that increase their expenses but don’t add income.

Consider that “money earning money” is your business. Your profession is how you draw a salary. Your business is how, independent of you, your money makes more money.

- Rich Dad, Poor Dad uses McDonald’s as a surprising example. McDonald’s isn’t a hamburger business - it’s in the real estate business. The profession is selling hamburger franchises, but the business is accumulating income-producing real estate.

Achieving Financial Independence

You might have the goal of financial independence, which is to no longer be dependent on your wages. Ideally, you can live forever off of the extra income your money generates - you make more money doing nothing than you consume.

The basic steps for financial independence are:

- Figure out how much money you need per year to survive.

- Figure out how much in assets you need, to generate a return that exceeds the first number (after taxes and expenses).

- Acquire assets that return that amount.

Even if your goal isn’t financial independence, these are still good principles of how to get the best return for your money.

So it’s that simple. But simple doesn’t mean easy. The major blocks are:

- psychological, where people fear the risk of higher-returning assets

- tactical, where people don’t know how to execute well

The rest of this Rich Dad, Poor Dad summary covers both obstacles.

Lesson 2: Buy Assets, Not Liabilities

So how do you put your money to work for you? The key is to buy things that generate income (assets). You do NOT want to buy things that lose money over time or incur large expenses (liabilities).

This is obvious enough. But the most deceptive investments look like assets, but are actually liabilities.

Liability: Buying a House as a Primary Residence

In Robert Kiyosaki’s view, the most common mistake is buying a house as a primary residence, and considering it an asset and their primary investment.

His reasoning:

- You don’t get rental income on your house. Meanwhile, you’re paying large expenses - mortgage, property taxes, upkeep. In steady state, this represents monthly negative cashflow that requires income to compensate. (Shortform note: Kiyosaki basically considers things assets only if they generate cash.)

- This is why many are stuck in the rat race - someone buys an expensive house. Now she has high monthly expenses, so she has to keep working to sustain it. Yes, the house may be appreciating, but that doesn’t help her high month to month expenses.

- The money tied up as a down payment, building up home equity, and paying expenses has a large opportunity cost. That money could be better spent on higher returning assets.

- While real estate can appreciate over the long term, there’s no guarantee of this.

- Even if real estate appreciates, you get the gain only on liquidation. (Kiyosaki seems to prefer investments with clearer short-term outcomes.)

- Considering your house as your primary investment causes a few subtle problems:

- People tend to overspend on housing, depleting money that could be spent on other investments.

- Because your cash is spent on the house, you never have enough money to think about what to do with it. This prevents building up the financial education to become a sophisticated investor.

- (Shortform note: also, loading too heavily on your house concentrates risk on your local real estate market. And if you’re subject to groupthink, you’re more likely to think buying a house is a great deal precisely when it’s actually not.)

- Many people buy a new house every number of years, each time incurring a new 30-year loan without really truly owning the house.

Shortform Explanation

Kiyosaki doesn’t address that people obviously have to live somewhere, and paying rent would also be an expense. And, typically, the monthly mortgage payment is lower than the monthly rent of the home, which is where people often get tripped up.

A proper analysis would compare the long-term outcome of these two options:

the cost of buying a home, including the down payment, annual expenses, and likely appreciation of home value

renting an identical property, increases in rental costs in proportion with home value appreciation, and investment returns of the extra cash from not buying a home (e.g. down payment) over time

But Rich Dad, Poor Dad isn’t great about these tactical details - one of its major failings. Going through the exercise, neither option is a clear home run, depending on your assumptions of how the housing market and stock market change.

So to bring it all together, here’s the best advice we imagine Kiyosaki would give:

As a mindset, don’t consider your home as your natural biggest investment. There are better places to put your money with better returns and more robust diversification.

Buy only the house that you need.

Do not overspend under the delusion that it’s going to be a great investment, or your major investment.

Do not buy to keep up with the Joneses - the money you save can be better employed elsewhere.

If you get a pay raise, don’t upgrade your house if you don’t need to. This is the cause of the vicious cycle putting you in the rat race.

Liability: Buying Expensive Stuff

Don’t buy physical goods whenever you get more money, with the expectation they’ll be good investments. This includes bigger houses, fancier cars, house renovations, handbags, jewelry, and golf clubs.

Not only do consumption goods not generate income, they also depreciate incredibly quickly.

- Common advice: A new car loses 25% of the price once you drive it off the lot.

- Corollary: buy used goods instead of obsessing about it being new.

Be especially careful when buying the thing just causes you to go further into debt. This is a major way to increase expenses without increasing income, thus digging you into a deeper hole.

- People have a tendency to spend money when they get it. But it’s not about how much money you make, it’s how much money you keep.

- More money only accentuates the cashflow pattern running in people’s heads. This is why giving people more money without financial education rarely improves their situation.

Kiyosaki isn’t saying don’t enjoy yourself. You can still buy nice things and live life well. But ideally, afford your luxuries using extra cash flow from your assets. This way you’ll feel like you’ve really earned it. Rich people buy luxuries last.

Assets

So what are real assets?

- Businesses that don’t require your presence. You own them, but they’re managed by other people. If you have to work there for it to generate money, it becomes your job.

- Only start a business if you have a desire for it. The odds are against you and the stress is high. You don’t have to make money this way.

- Stock, bonds, funds, and other securities.

- Kiyosaki once liked tax liens, which he claims returned 16%, but says since then more attention has made this less profitable.

- Income-generating real estate. In particular:

- Using debt to lever up on more houses. In other words, with $500k, you could buy one $500k house and use it to make income. Or, you could pay $100k down payments for 5 houses and get rental income from 5 houses.

- (Shortform caveat: note that with more leverage, if the houses lose value, you also magnify your losses, as in the 2008 recession.]

- Buying under-market properties, like from foreclosures, and reselling them quickly.

- Kiyosaki notes that today foreclosures are competitive and he’s looking elsewhere.

- Using steady cash flow from rental income to make riskier bets, like in the stock market.

- Consider buying property that’s larger than what you need. Then sell off a piece to someone else. This will let you broaden the opportunities you find.

- When selling a property, trade it for a larger one to avoid immediate taxes on the gain. (Section 1031)

- Using debt to lever up on more houses. In other words, with $500k, you could buy one $500k house and use it to make income. Or, you could pay $100k down payments for 5 houses and get rental income from 5 houses.

- Notes (IOUs).

- Royalties from intellectual property such as music, scripts, patents.

- Anything that has value, produces income, appreciates, and has a ready market.

(Shortform note: Rich Dad, Poor Dad contains lots of (possibly embellished) examples of super-profitable real estate deals. Unfortunately the book doesn’t cover how to find or generate valuable assets, which is a much more complicated topic and specific to the industry.)

Think about each dollar as your employee that works 24 hours a day tirelessly to make you more money.

The tradeoff between today’s expenses and future income should be clear. Every dollar you spend today is a dollar that does not work for you again, in perpetuity.

Further, avoid situations where you have to dip into savings or investments. Find creative ways to come up with the money, and protect your assets.

Pay Yourself First

Most people have the habit of paying their bills first, then saving whatever money is left.

Rich Dad inverted this - he bought assets first, then paid his bills as late as possible. His reasoning - the threat of having bill collectors was supremely strong motivation to creatively find ways to make more money.

In contrast, paying yourself last gives little pressure to generate more money.

Lesson 3: Reduce Taxes Through Corporations

(Shortform caveat: we consider this the worst chapter in the book. He doesn’t explain the advice clearly enough to be useful. The advice doesn’t apply to most people’s situations. And taken incorrectly, it could get you into trouble.

Treat none of this as actual tax advice; seek a tax attorney for real advice, and executing some of this too liberally is illegal.)

Why Taxation is Bad

In Rich Dad, Poor Dad, Robert Kiyosaki is clearly strongly against taxation, saying things like:

- Most people work from January to May just for the government.

- The Social Security tax is an insidiously large tax, at 15% of wages.

- Originally in England/early US, taxes were only levied against the rich. They were then extended to middle and lower classes to support a growing government appetite for money, and eventually taxation disproportionately punishes the poor.

- The biggest bully isn’t your employer or your manager, but the tax man. “The tax man will always take more if you let him.”

Whatever your philosophical bent on taxation, the practical point is that the rich find ways to minimize their tax burden, sometimes paying a lower % of their income than lower tax brackets.

Forming a Corporation

Robert Kiyosaki’s solution? Form your own corporation. Here are its benefits:

Deductions for Expenses

You can pay legitimate business expenses from pre-tax money, rather than post-tax money.

Say you have a business that buys and sells real estate. To travel to see new properties, you can pay for a car. You have business dinners that you can partially expense. You can have board meetings in exotic locations you would have vacationed anyway.

Shortform Explanation

Here’s the financial difference.

Say you earn $100 from salary, and after 40% taxes it’s $60 in your pocket. Your car costs $60, so you end up with $0.

Say your corporation makes $100 in income. Your car is used for business, so the corporation pays $60 for the car. The corporation then has income of $40. After a 40% tax, this ends up being $24. This profit can then be distributed to shareholders as a dividend.

- (In reality, this would be taxed at a 20% corporate rate and 20% personal capital gains rate, but I use 40% to better compare with the pre-tax situation above)

Here’s another way to phrase it: In the company, the $60, if it wasn’t spent on the car, would have been taxed as income. After the 40% tax, this is equivalent to $36. So it basically cost you $36 post-tax to get the car service, rather than $60 pre-tax, leading to a $24/$60 = 40% discount.

Again, be very careful with this. This isn’t a limitless buffet that you can transfer all personal expenses to. Make sure you understand what counts as a legitimate business expense and what creeps across the line to personal expenses.

Lower Tax Rates (allegedly)

From the book: “the income-tax rate of the corporation is less than the individual income-tax rates.”

Shortform Explanation

Superficially, this is true: in 2017 and before, corporate income tax used to be a flat 35%, while personal income tax was 39.6% at the highest bracket. In 2018, this became 21% and 37% respectively.

What he ignores, though, is that the corporate income is paid out to shareholders through dividends, which incurs an additional 20% personal capital gains tax.

Therefore the actual tax rate on dividends is now 1 - 0.79 * 0.8 = 36.8%, only slightly better than 37%.

Protection from Lawsuits

Corporations and trusts can protect assets from creditors. A rich person as an individual may control things but own nothing.

(Shortform caveat: though in certain cases (like fraud or the corporation being essentially the same as the person), a litigant can “pierce the corporate veil” and hold you individually responsible.)

Delaying Taxes on Real Estate Sales

Take advantage of Section 1031, which allows delaying taxes on real estate that is exchanged for a more expensive piece (in a delayed exchange, you have 45 days to find a replacement property and 180 days to complete the sale).

Lesson 4: Overcome Your Mental Obstacles

More people have the potential to be happy, but common obstacles get in the way. People who overcome these obstacles get a huge advantage.

Self-Doubt

Self-doubt or lack of self-confidence hold all of us back, to some degree. Some are affected more than others.

In the real world, more than just intelligence and grades is required. Guts, chutzpah, balls, daring, tenacity, grit are different names for the factor that plays a huge role in success.

When you recognize a great opportunity, you must have the courage to chase it.

(Shortform example: a quote from Charlie Munger: “We read a lot. But that’s not enough: You have to have a temperament to grab ideas and do sensible things. Most people don’t grab the right ideas or don’t know what to do with them.”)

Fear

Fear manifests in a lot of ways.

Fear of Losing or Failure

Fear of losing makes you play it safe and avoid opportunities that can have huge upsides and relatively low downsides. Control your fear of losing, money or otherwise. Everyone has fear of losing money, but you have to handle it properly.

- (Shortform note: This is well rooted in psychology - losses are more painful than equivalent gains. See Kahneman’s Thinking, Fast and Slow.)

School teaches us that mistakes are bad, but this is terrible for real life. Winners aren’t afraid of losing, but losers are. People who avoid failure also avoid success.

Every rich person has lost money. Someone who has never lost money is probably not rich.

Winning requires being unafraid to lose.

Failure will only make you stronger and smarter. Take a loss and make it a win. Use your failure to inspire yourself to become a winner. For winners, losing inspires them. For losers, losing defeats them. Use this sentiment to lower the perceived cost of failing.

Rich Dad says he like Texans, because “when they win, they win big. And when they lose, they lose big, and it’s spectacular. If you’re going to go broke, go big. Don’t admit you went broke over a duplex.” Even though the South lost at the Alamo, they handle failure fondly, shouting, “Remember the Alamo!”

(Shortform caveat: of course, taken to the extreme with an uninformed person, this can cause excessive risk taking and catastrophic losses.)

Fear of Risk

Don’t be afraid of turbulence or risk. “I’d like to, but I’m due for promotion in three months” is the classic excuse. There is always another carrot dangled ahead of you, and so there’s always a good reason not to do what you really want to do.

Fear of Rejection

Don’t be afraid of rejection. Fear of ostracism prevents people from having nonconsensus opinions. As it relates to finance, it’s in 1) not bucking the consensus traditional way of handling your career and money, 2) keeping up with the Joneses and matching spending. Focus on yourself and your personal goals, regardless of what other people think.

If you fear all of these things, you can still be rich. But it requires a wiser, more conservative path: start young, save money, and use compound wealth to become rich when you’re old.

Cynicism

There will always be at least one reason something won’t work. Fixating on these reasons pessimistically will paralyze you from taking any productive step.

Common meaningless rebuttals:

- What if things don’t go as planned?

- What makes you think you can do that?

- If it’s such a good idea, how come someone else hasn’t done it?

- That will never work.

Use your analysis to find opportunities that critics are blind to. Remember, other people are blind to opportunities because they seek security and safety.

Laziness

Some people feel developing financial intelligence is too much hassle. Consider, would you rather put in some hard work now and enjoy decades of a better life, or suffer through the rest of life?

Counterintuitively, busy people are often the most lazy. They stay busy as a way of avoiding something they don’t want to face.

Consider someone who works all day and weekends to make ends meet, without confronting bigger problems like how to build wealth or their family’s well-being. They can brush off investment opportunities as, “I’m working hard enough as it is, and my boss wants me to do more work. I don’t have the time.” In reality, they don’t want to push themselves to do the harder thing of figuring out novel, less-obvious solutions to getting more money.

Forcing yourself to think about how to make more money is like exercising at the gym. The more you work your mental money muscles out, the stronger you get.

Corollary: Find areas that people don’t to work in, and there are likely unclaimed opportunities there.

- People often don’t want to invest in real estate because they don’t want to fix toilets. Their loss is your gain. And in reality, you can hire a property manager to handle the physical work.

Feeling Guilt for Being Greedy

We’ve been raised to think of greed or desire as bad. “Stop thinking about yourself. Why don’t you think about others?”

In reality, self-interest (generally, wanting to make your own life better) drives innovation and value for other people. This is the cornerstone of capitalism.

Condemning greed might be a trained defense, learned helplessness. “I don’t know how to become rich. So I’m just going to try to believe being rich is bad, and there’s valor in not wanting to be rich. Even though secretly I would love to be rich.” It’s easy to imagine parents feeling this, then teaching it to their kids.

Arrogance

“If you want to improve, be content to be thought foolish and stupid.” –Epictetus

Arrogance is ego plus ignorance.

When you’re ignorant in a subject, recognize this, then educate yourself.

Intelligent people welcome new ideas, since new ideas add synergy with other ideas.

Don’t be afraid of people smarter than you. Find out how to get them to work with you.

Don’t feel a trade is underneath you. Some people have an allergy to learning sales techniques, without realizing that much of the world runs on sales of some sort.

Lack of Money

Many people don’t even start their pursuit with the excuse that they don’t have the money. This doesn’t stop the courageous opportunist from making progress.

Robert Kiyosaki shares how he bought an apartment complex without money by writing a contract between seller and buyer, and basically earning a finder’s fee for the transaction.

Lesson 5: Keep Learning All the Time

Developing financial intelligence pays off huge returns. If your mind is trained well, you can create enormous wealth in what in the grand scope of things is an instant.

In contrast, an untrained mind can also create poverty that lasts lifetimes.

Robert Kiyosaki believes financial intelligence is made up of four broad areas of expertise:

- Accounting: financial literacy. Read and understand financial statements.

- Investing: strategies to use money to make more money. The creative piece.

- Understanding markets: understand supply and demand. Can you create something that the market wants? Does an investment make sense under current market conditions?

- Law: use tax advantages and legal protection to build wealth more quickly and reduce risk.

Taken together, financial intelligence allows you to construct creative ways to solve financial problems, vet the ones that are more likely to work, then have the technical ability to execute them.

Consider that spending money on financial intelligence is like buying yourself life - you may save on years of working because of making the right decisions.

Keep Learning, and Learn Quickly

Great opportunities arise in a changing world. (Shortform note: Put technically, markets are less efficient and less at equilibrium when things rapidly change, like through new technology.)

300 years ago, land was the basis of wealth. Then factories and industry became the new basis for wealth. Today, it’s information. And by its nature, information changes more rapidly than land or manufacturing. So it’s even more important to keep learning and adapting, quickly, as it’s ever been.

(Quote from Charlie Munger: “In my whole life, I have known no wise people (over a broad subject matter area) who didn’t read all the time — none, zero. You’d be amazed at how much Warren [Buffett] reads.”)

This doesn’t have to be difficult or intense. Robert Kiyosaki mentions jogging through his neighborhood to spot which houses were listed for sale for longer than others, and making low-ball offers for these houses.

The more you learn and the more experience you get, the more money you make, which gives you more chances to learn even further. The faster you can iterate your knowledge, the faster the returns compound.

Learn Broadly

Many people with great talent in their trade aren’t rich. They’re specialists and proud of it.

Often, they just need to learn and master one more skill to dramatically boost their income.

- Analogy: How many people can make a better hamburger than McDonald’s? Most people would think so. Then why does McDonald’s make more money than they do? Because McDonald’s has mastered a business system, while most people focus on building a better hamburger.

Notable examples of underappreciated skills include sales, marketing, communication, negotiating, investing, people management, and financial intelligence.

- Consider taking a pay cut to work at a firm where you’ll gain a critical orthogonal skill - like marketing at an ad agency, or people leadership in the military.

- Rich Dad invited his son and the author to work in a broad set of roles at his companies (bus boy, construction worker, accounting) and participate in meetings with bankers, lawyers, and accountants.

Look ahead at what skills you want to acquire before choosing a profession and specializing in the rat race.

Side note: if you do specialize instead of generalize, make sure you have a union. If your specialist skills are of limited value outside the industry, like teachers or airline pilots, you’ll have nowhere to work if you get pushed out of the industry.

Lesson 6: How to Get Started

Finally, we’ll end with tips on how to get started on your path to building wealth:

1. Need a reason greater than reality.

Find a deep reason you want to succeed. This is usually a combination of “wants” and “don’t wants.”

Examples: “I don’t want to work all my life. I don’t like being an employee. I hated that my dad missed my football games since he was obsessing about his career. I want to be free to travel the world when I’m young. I want control over my time.”

If you don’t have a strong reason, you won’t make it. It will sound like too much work.

2. Actively choose to be rich and think every day.

Ask, what would a rich person do in this situation?

Invest in educating yourself.

3. Choose friends carefully. Consciously make effort to learn from them.

Don’t seek people for their money. Seek them for their knowledge.

Find someone who has done what you want to do. Take them to lunch.

Don’t listen to frightened people who always advice caution or are pessimistic. They drag you down.

Funnily, rich people have friends who ask them for jobs or a loan, but rarely to ask them how they made money.

4. Master a formula (a way to make money) and then learn a new one.

Formulas lose their potency as they become more common. Keep reinventing yourself and finding new ways to create value.

5. Pay yourself first.

As described above, buy your assets first, and pay the bills last. The pressure will force you to creatively think of ways to generate more money.

Importantly, this doesn’t mean don’t pay bills, or to incur greater debt. Don’t get yourself into debt in the first place.

Don’t dip into your savings or investments. Protect your assets when the going gets tough.

6. Pay your advisors and brokers well.

They provide valuable information and take time to educate you.

Hire professionals who know what they’re talking about, and have skin in the game. An attorney who personally invests in real estate will be more helpful for your real estate matters.

Don’t short-change your brokers. Why would they want to hang around you if you’re not being fair?

You’ll be comfortable paying them better when you value your time and understand the value of what they give.

7. Buy assets that generate free money.

Find a way to put in money and get it back, then get free money into the future. Kiyosaki relates this to “Indian giving.”

Example: Buy a cheap house with cash, use rent to pay it off, and the house now generates money forever.

Sophisticated investors ask, “how fast do I get my money back?”

8. Buy luxuries with income from assets only.

You must resist the temptation to spend any extra money you get. This requires fortitude.

Do NOT borrow money to get the things you want. Focus on creating money.

9. Find your personal hero. Emulate their behavior.

Learn how they make decisions, and how they got to where they are.

When negotiating, Kiyosaki “acts with the bravado of Trump.”

Heroes who make it look easy convince you to be just like them. “If it’s easy for them, I can do it too.”

10. Give to others first, and it’ll come back many times over.

This is true for money, a smile, love, friendship.

Help someone sell something, and sales will come to you.

Trust that reciprocity will work its way back.

Parable: a man is sitting in front of a stove with firewood in his arms on a freezing night. He yells, “when you give me some heat, then I’ll put some wood in!”